Equity management

Equity management

ESOP Management

ESOP Management- Fund management

Liquidity Solutions

Liquidity Solutions - Fund managementESOP Consulting

- Fund managementFund Management

Designing a Phantom Option Plan for an NBFC

Every funding round, every option grant, and every convertible instrument signed restructures a company's equity structure, often in ways that a basic cap table does not immediately reflect. Fully diluted shares account for all of that, presenting the total number of shares that could exist once every potential security is exercised or converted.

For founders approaching fundraising, investors evaluating ownership stakes, and employees assessing the value of their equity, fully diluted shares are the most complete and accurate measure of a company's ownership structure. This guide breaks down what fully diluted shares are, how they are calculated, and why it is important at every stage of a company's growth.

Fully diluted shares represent the total number of shares a company would have outstanding, including both shares currently held by shareholders and all potential shares that could be created through the conversion or exercise of instruments such as preference shares, stock options, warrants, SAFEs, and convertible notes.

Fully diluted shares are built from several financial instruments, each representing shares that could exist in the future. The most common instruments included are:

1. Stock options: Stock options granted to employees or executives are included in the fully diluted share count because they represent shares that could exist in the future. The mechanism is straightforward, when an employee exercises their option at the predetermined exercise price, the company issues new shares, increasing the total share count. Even before exercise, these options are factored into the fully diluted count to give a complete picture of potential ownership.

2. Warrants: Warrants issued to investors or lenders work similarly to stock options, they give the holder the right to buy into the company at a fixed price within a defined timeframe within a set period. When a warrant is exercised, the company issues new shares to the holder, directly increasing the fully diluted share count. Since they represent potential equity, excluding them would understate the true share count.

3. Convertible note: A convertible note is a form of debt financing that is designed to turn into equity at a future point, usually at a discount to the next funding round's valuation. The shares it would produce upon conversion are factored into the fully diluted share count from the moment the note is issued.

4. SAFEs: A SAFE, or simple agreement for future equity, allows investors to provide capital upfront with the understanding that they will receive equity at a later stage, typically triggered by a funding round or liquidity event. Since a SAFE will eventually convert into shares, the number of shares it would produce upon conversion is included in the fully diluted share count even before that conversion occurs.

5. Preference shares: Preference shares sit above common stock in the ownership hierarchy, giving holders priority in dividends and liquidation events. Most preference shares issued to investors carry a conversion right, allowing them to convert into common stock at a predetermined ratio. When converted, they increase the total share count and are therefore included in the fully diluted share count.

Once the fully diluted share count is established, it directly influences two key financial metrics that every stakeholder should understand

Every time a company issues new shares, the total number of shares outstanding increases, directly impacting the fully diluted share count. Several events can trigger an increase in the fully diluted share count:

1. Fundraising rounds: When a startup raises capital and issues new shares to investors, those shares are immediately reflected in the fully diluted count. Additionally, new investors may require the creation or expansion of an option pool as part of the round, which further increases the fully diluted share count even before those options are granted or exercised.

2. Employee option pools: When a company creates or expands an employee option pool, all reserved shares, including unvested and unexercised options, are added to the fully diluted share count. This is because fully diluted shares account for all shares that could potentially exist, not just those currently active.

3. Going public (IPO): At the time of an IPO, all previously issued options, warrants, and convertible instruments are typically converted or exercised, significantly increasing the fully diluted share count. Post-IPO secondary offerings add further shares, expanding the count even more.

Here is a step-by-step process to calculate fully diluted shares

1. Start with basic shares outstanding. This includes all issued shares currently in circulation.

2. Identify convertible securities: Stock options, warrants, convertible debt, and preferred shares.

3. Apply the treasury stock method (for options): Calculate the additional shares created accounting for any repurchased shares using the exercise proceeds.

4. Add all securities: Combine the basic shares with those from convertible securities to determine the fully diluted share count.

Fully Diluted Shares = Number of Common Shares Outstanding + Convertible Securities + Stock Options + Warrants + The Option Pool

Hypothetical example of fully diluted shares

Let's consider a company with:

Calculation:

The fully diluted share count becomes 1,600,000 shares. This total provides a more comprehensive understanding of the company's equity structure.

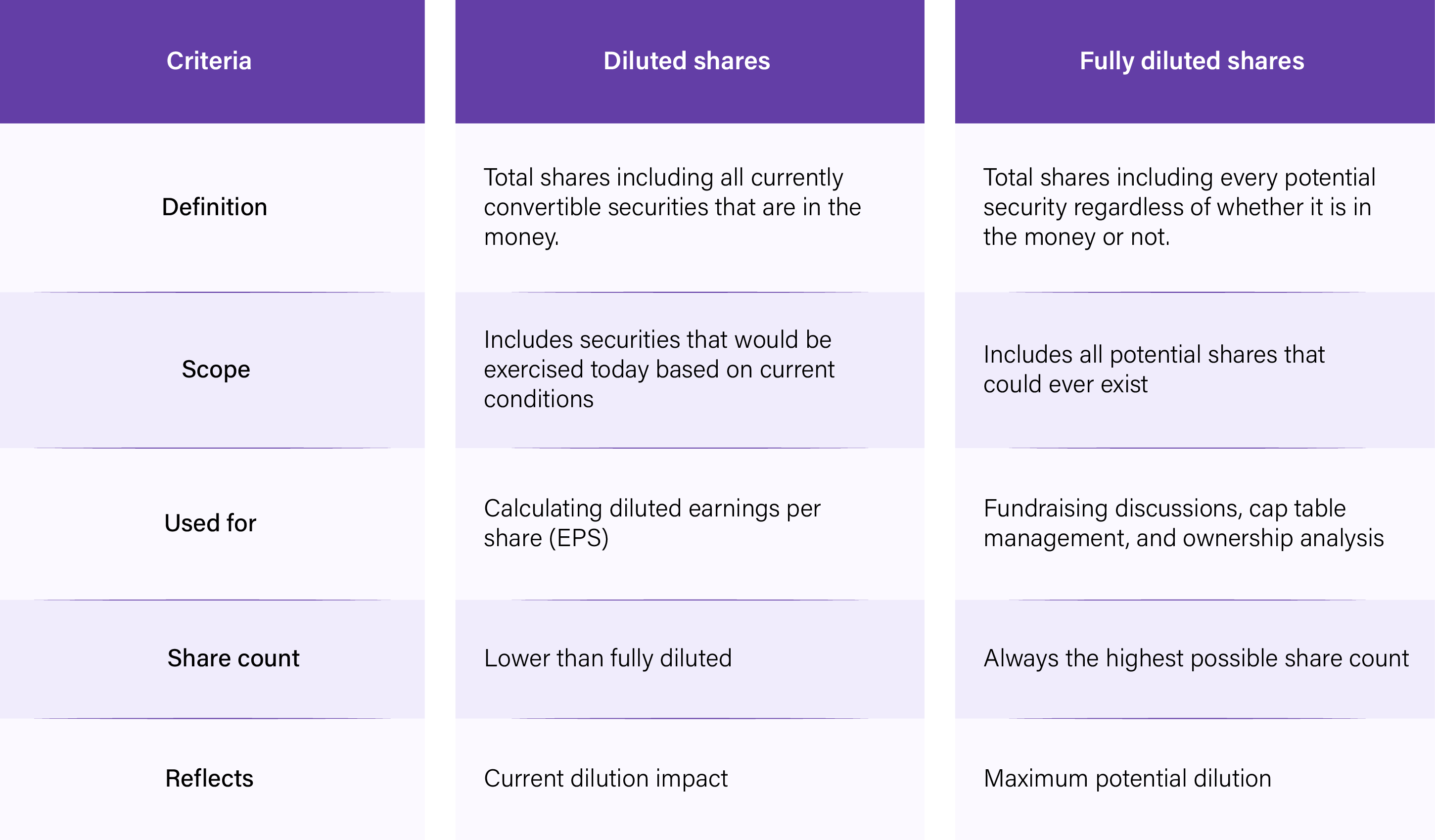

Many founders and employees use these two terms interchangeably, but they are not the same. Understanding the difference is important before diving into a broader comparison of share types.

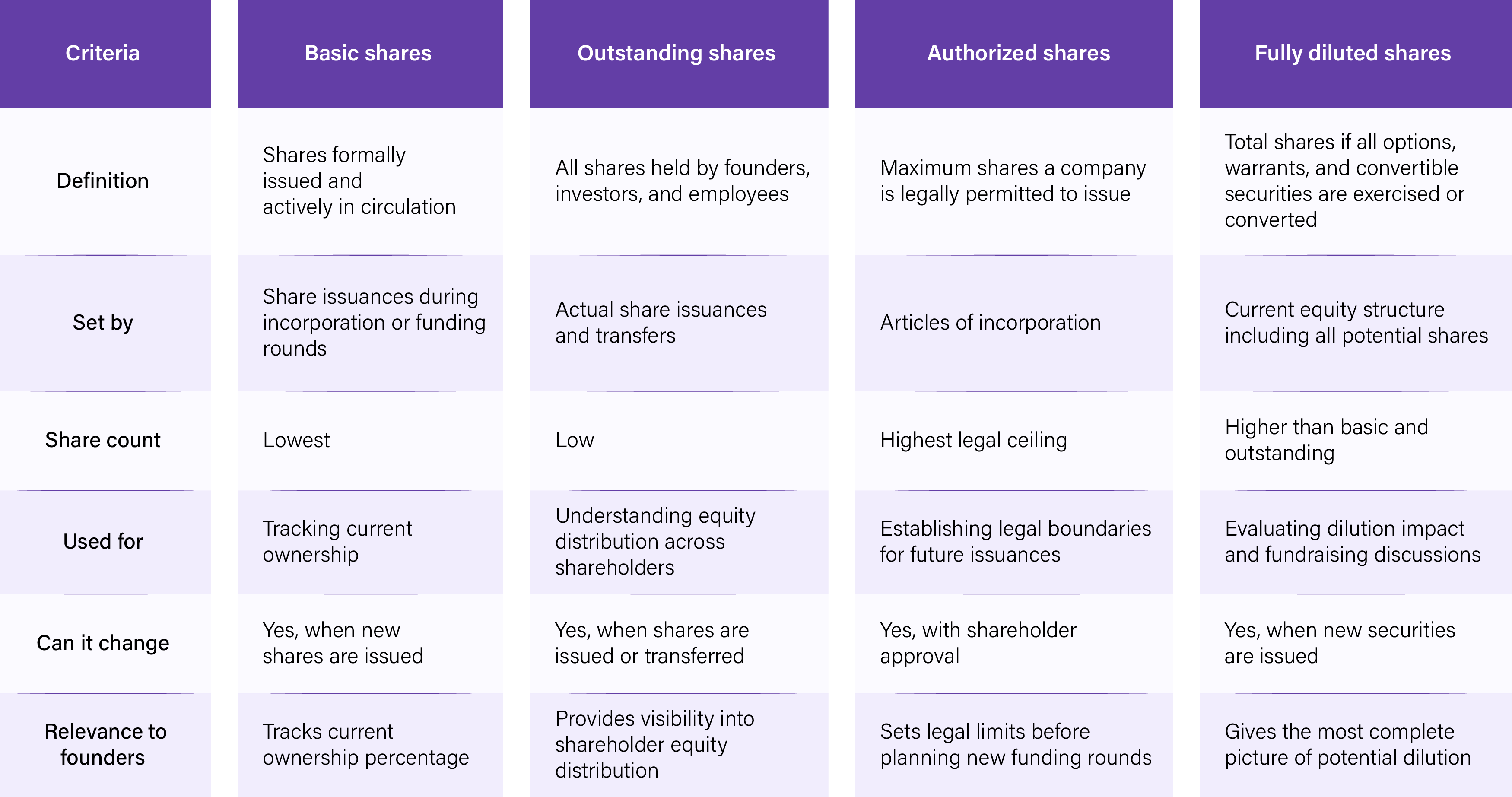

Now that we understand how fully diluted shares differ from diluted shares, let us look at how it compares to other share types that founders and investors commonly encounter

Managing fully diluted shares effectively requires the right processes and tools in place. Here are some practical steps to help founders and finance teams stay on top of their equity structure

1. Use Cap Table Management Software: Use Qapita's platform to track equity structures, manage stock options, and calculate fully diluted shares seamlessly.

2. Regularly Update Your Cap Table: Ensure that your cap table reflects the latest share issuances, option grants, and conversions. This helps you maintain transparency with stakeholders and avoid surprises during funding rounds or audits.

3. Analyze Dilution Scenarios: Use financial modeling to predict the dilutive effect of issuing new shares. Run "what-if" scenarios to evaluate how different funding or equity compensation decisions might impact ownership percentages and financial metrics.

4. Consult Legal and Financial Experts: Getting familiarized with complex instruments like convertible debt or preferred shares can be challenging. Consult a legal and financial advisor to ensure compliance and accuracy in your calculations.

Fully diluted shares provide a clear view of a company's potential ownership structure, making them an essential metric for stakeholders. Employees need to understand how their stock options might be affected by dilution, while investors assess risks and opportunities in valuation. Companies must carefully balance the issuance of new shares to grow without excessively diluting ownership. Using accurate calculations and the right tools, companies can maintain transparency with all stakeholders and make informed equity decisions at every stage of growth.

Every funding round, option grant, and convertible note changes your equity structure. Before you walk into investor negotiations, you need to know exactly what your fully diluted share count looks like, and how it will change after the round closes. Qapita's cap table platform lets you model dilution scenarios, track all potential shares in one place, and walk into every funding conversation fully prepared.

Book a demo to see how Qapita can help.

Fully diluted shares are neither good nor bad, they are a metric that reflects the complete picture of a company's potential ownership structure. A higher fully diluted share count signals greater dilution for existing shareholders, but if the capital raised drives significant growth and increases the company's overall valuation, the dilution can be worthwhile. The key is understanding how each new issuance impacts ownership before committing to it.

Basic shares refer to the total number of shares currently issued and actively in circulation. Fully diluted shares go further by including all potential shares that could exist if every outstanding option, warrant, SAFE, convertible note, and preference share were exercised or converted. The fully diluted share count is always higher than the basic share count and gives a more complete picture of ownership.

Consider a company with 1,000,000 basic shares outstanding, 300,000 stock options, 100,000 warrants, and convertible debt that converts into 200,000 shares. If all these securities were exercised or converted, the fully diluted share count would be 1,600,000 shares. Each existing shareholder's ownership percentage would be calculated against this higher number, reflecting the true extent of dilution.

Yes, fully diluted shares include unvested options. This is one of the key distinctions between fully diluted shares and other share count metrics. Since fully diluted shares are designed to reflect the maximum possible number of shares that could ever exist, all options are included, whether vested, unvested, or unexercised. Unvested options represent shares that could be created in the future once the vesting conditions are met, making them a relevant part of the fully diluted share count

Fully diluted shares are calculated by starting with the basic shares outstanding and adding every potential share that could be created through the exercise or conversion of outstanding securities.

The formula is:

Fully Diluted Shares = Number of Common Shares Outstanding + Stock Options + Warrants + Convertible Securities + The Option Pool

.webp)