Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

As a startup founder, one of the significant benefits you can provide to your team is the opportunity to purchase company stock at a discount or with tax benefits. Various employee stock purchase plans provide these features and allow employees to contribute payroll deductions towards purchasing company stock, often at a price lower than the Fair Market Value (FMV). Such types of employee stock options are usually available for all team members, from the C-suite executives to the support staff.

However, there is another category of stock options, referred to as Incentive Stock Options (ISOs). These options are generally reserved for key employees and upper management. Also known as statutory or qualified options, they offer preferential tax treatment in various situations, making them a useful tool for attracting and retaining top talent.

This blog covers the important aspects of ISOs, including their types, benefits, challenges, vesting and holding periods, and taxation treatment. Keep reading to learn more.

ISOs are a form of equity compensation that you, as a startup founder, can grant to your employees. They offer your team the opportunity to purchase company shares at a discounted price, aligning their interests with the success of your startup.

ISOs differ from NSOs in several ways, primarily in terms of eligibility and tax treatment. While NSOs can be granted to anyone, ISOs are typically reserved for employees. Moreover, ISOs offer potential tax advantages, such as the eligibility for long-term capital gains tax treatment, which can result in lower tax rates for your employees.

Here are some of the most important features of ISOs:

Here is a comparative analysis to help you understand these two types of stock options better:

Two critical timelines in the lifecycle of ISOs are the vesting period and the holding period. Here are some important details related to these periods:

The vesting period is a fixed timeline that determines when your employees gradually earn the right to exercise their ISOs. Typically spread over several years, this period is a way for you to ensure that your employees stay committed to your startup for a significant duration.

During the vesting period, a certain percentage of ISOs become 'vested,' meaning your employees earn the right to exercise these options and purchase company shares at the pre-determined price. Meeting the vesting requirements is essential for your employees to be able to purchase the shares and potentially benefit from the company's growth.

The holding period is another important timeline that begins once your employees exercise their ISOs and purchase company shares. To qualify for favorable long-term capital gains tax treatment, the employees must hold the shares for a certain period post-exercise.

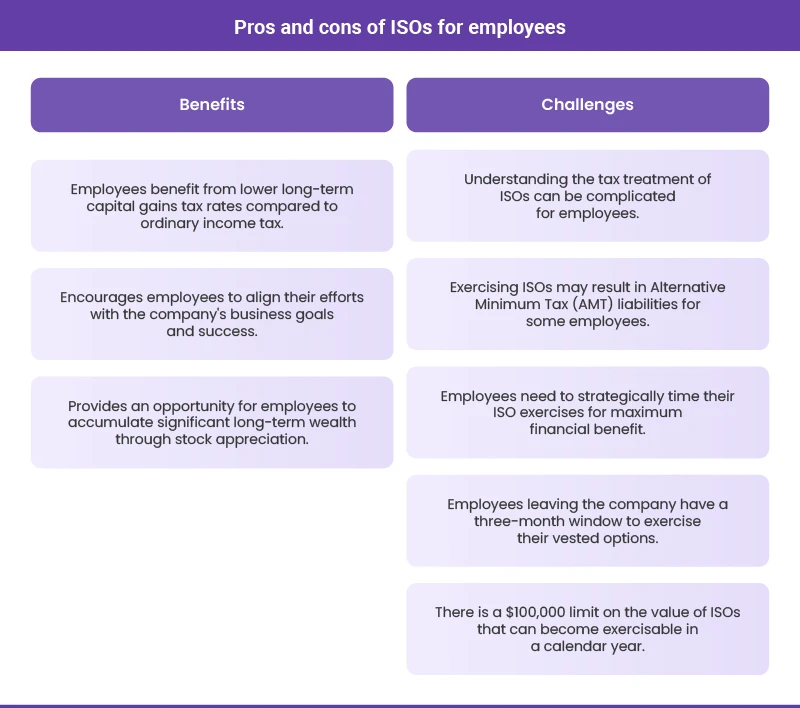

This holding period is typically two years from the grant date and one year from the exercise date. If your employees sell their shares before meeting these holding period requirements, the sale is considered a 'disqualifying disposition,' and they may lose the potential tax benefits associated with ISOs. In this scenario, their gains will be taxed as ordinary income rather than at the lower capital gains tax rates.

Incentive Stock Options (ISOs) work by allowing your employees to purchase company shares at a pre-determined strike price, which is often lower than the current market value. This difference, known as the 'spread,' can translate into significant financial gains for your employees.

However, the timing of exercising ISOs is crucial. If exercised too early, employees might face a hefty AMT. If exercised too late, they might miss out on potential gains from stock price appreciation. Hence, strategic decision-making is key to maximizing the benefits of ISOs.

Employees can exercise their Incentive Stock Options (ISOs) anytime during the vesting period, which is typically spread over several years. They cannot exercise their ISOs immediately upon grant; they must wait until the options have vested.

Upon exercising, they purchase company shares at a pre-set price, irrespective of the current market price. This transaction is a taxable event and may be subject to Alternative Minimum Tax (AMT).

The tax implications depend on when the employees sell their shares. Selling before the year-end may result in a mix of ordinary income and capital gain/loss taxes. Holding past the year-end could trigger AMT.

After exercising their ISOs, employees have options, they can sell the shares immediately, hold for potential future gains, or use them to optimize their tax situation. Each choice impacts their tax obligations and should be considered carefully based on their financial goals and market conditions.

Incentive Stock Options (ISOs) offer a range of benefits and challenges for employees, as discussed in this section:

Incentive Stock Options (ISOs) stand out as one of the popular employee stock purchase plans due to their potential for favorable tax treatment. However, to avail of these tax benefits, certain conditions must be met. There are two different variations of ISO dispositions:

Similar to non-statutory options, ISOs do not incur tax consequences at the grant or vesting stages; tax reporting is only required upon the sale of the stock. If the stock sale qualifies, the gains are generally taxable at the lower long-term capital gains rate instead of as ordinary income.

As per the filing status and taxable income for individuals, long-term capital gains tax rates are 0%, 15%, or 20%. Most individuals pay a maximum of 15% on their long-term capital gains, which is significantly lower than the ordinary income tax rates that can reach up to 37%, resulting in substantial tax savings for employees.

While qualifying ISOs can be mentioned in the IRS Form 1040 as long-term capital gains, the bargain element (variation between the exercise price and the FMV of stock) at the time of exercise is also a preference item for the AMT. This tax is applicable to individuals who have large amounts of certain income, such as ISO bargain elements or municipal bond interest. It has been created to make sure that every taxable individual pays some tax on the income that might otherwise be classified as tax-free. This calculation is completed using the IRS Form 6251.

If employees exercise a large number of ISOs, they must contact a tax advisor to determine the taxation aspects of their transactions. The amount realized from the liquidation of ISO stock needs to be mentioned in IRS form 3921 and then carried over to Schedule D. As a startup founder, understanding these tax implications is crucial for effectively managing your equity compensation strategy.

Navigating the complexities of ISOs can be challenging. As a startup founder, you need a reliable partner to help you manage these complexities. That's where Qapita can help.

Rated as the #1 Equity Management Software platform by G2, we at Qapita understand all the complexities of equity compensation. We have built a leading equity management platform that supports over 2,400+ fast-growing companies globally. Our software solution streamlines the equity management process around Cap Tables, ESOPs, and transactions. We also facilitate liquidity to ESOP holders and shareholders via structured buyback programs and secondary transactions.

Get in touch with our experts and learn how Qapita can help streamline the benefits for your stakeholders.

ISOs have potential drawbacks for startup founders. They only provide value if the stock price increases above the exercise price. If stock value declines or stagnates, ISOs can lose motivational power. Employees must pay the exercise price, which may require borrowing or selling shares. Determining fair market value for pricing can incur additional costs. Full tax benefits may not be realized if holding period requirements are not met.

Timing ISO exercise is crucial for startup employees. Consider exercising when the stock price is low to minimize the taxable spread. Hold shares for at least a year after exercise and two years from the grant date to qualify for long-term capital gains rates. Evaluate your financial situation and the company's prospects. Remember, ISOs must be exercised within ten years of the grant date or earlier if employment terminates.

In an acquisition, ISO treatment can be affected. Merger agreements often allow for accelerations upon a change in control, potentially vesting unvested options. The acquiring company typically assumes outstanding options. However, vested and exercised options need consideration when determining the $100K limit for accelerated ISOs. This may require additional steps to correctly split outstanding ISO awards between ISOs and non-qualified stock options.

ISOs are exclusively granted to employees of the corporation issuing the options or certain related corporations. Non-employee service providers, such as independent contractors, non-employee board members, or consultants, are not eligible for ISOs. The option must be granted under a formal written plan approved by shareholders, specifying the maximum number of shares issuable as ISOs and the class of eligible employees.

The tax rate on ISOs depends on how long the shares are held. If held for at least one year after exercise and two years after grant, the entire gain is taxed at long-term capital gains rates. If sold earlier (a disqualifying disposition), the difference between exercise price and fair market value at exercise is taxed as ordinary income. Any additional gain is taxed as capital gain, either short-term or long-term, depending on the holding period.

-min.png)