Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Stock options are a popular form of compensation for employees, particularly in startups and other high-growth companies.

Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) are common types of stock options that companies offer to their employees. While both types of options provide employees with the opportunity to purchase company stock at a discounted price, there are significant differences between the two.

In this article, we will explore the differences between ISOs and NSOs, their tax treatments, and their implications for employees and startups.

Incentive Stock Options (ISOs) are a type of stock option granted to employees as part of their compensation package. ISOs are typically offered to key employees, such as executives and managers, and are designed to incentivize them to work towards the long-term success of the company. ISOs are subject to specific rules and regulations under the Internal Revenue Code, which govern their tax treatment.

Non-Qualified Stock Options (NSOs), on the other hand, are a type of stock option that is not subject to the same rules and regulations as ISOs. NSOs are typically offered to a broader range of employees, including rank-and-file employees, contractors, and consultants. NSOs are not subject to the same tax treatment as ISOs, and their tax implications can be more complex.

Non-qualified stock options (NSOs) are employee stock options that do not carry preferential tax treatment. Upon exercise, the difference between the exercise price and the market value of the stock is taxed as ordinary income.

It is essential for employees and startups to understand the differences between ISOs and NSOs, as they can have significant implications for tax treatment and potential benefits. For employees, understanding the differences can help them make informed decisions about their compensation packages and maximize their potential benefits. For startups, understanding the differences can help them design compensation packages that are attractive to employees while minimizing their tax liabilities.

ISOs and NSOs work in similar ways, in that they both provide employees with the opportunity to purchase company stock at a discounted price. However, there are significant differences in their tax treatment and eligibility requirements.

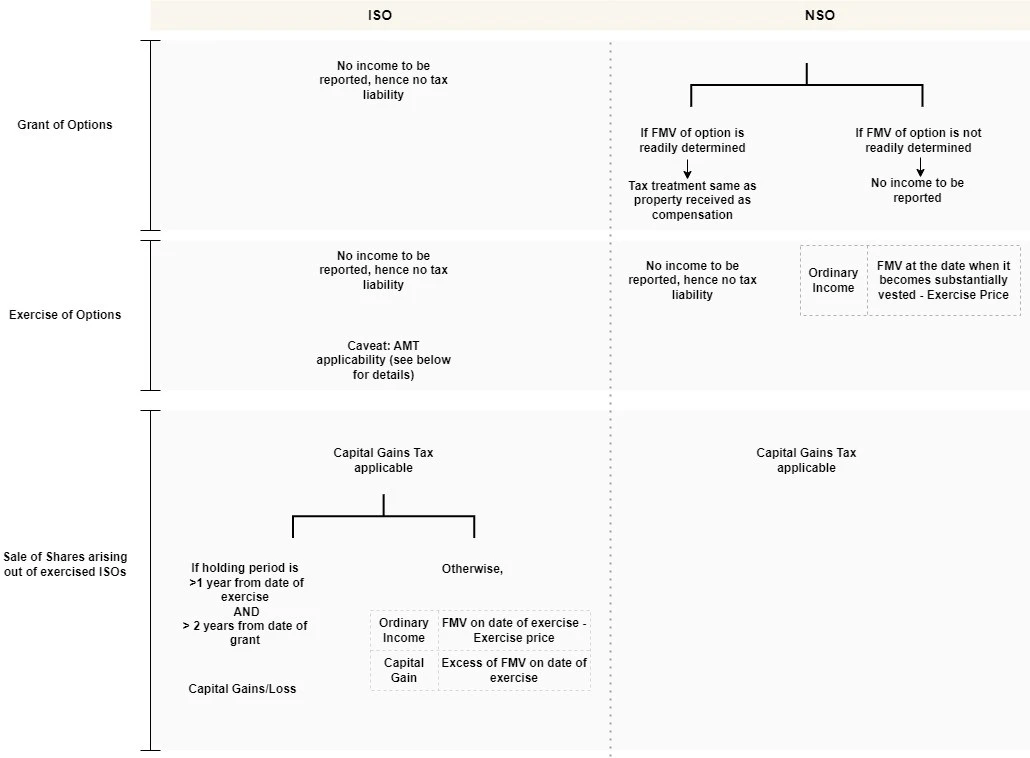

Incentive stock options (ISOs) are governed by specific Internal Revenue Code provisions that determine their tax treatment. To qualify, employees must meet certain conditions, such as meeting minimum service requirements and not holding more than 10% of the company's ownership. Additionally, ISOs are typically subject to a vesting schedule, requiring employees to wait a defined period before exercising their options.

NSOs, on the other hand, are not subject to the same rules and regulations as ISOs. NSOs are typically offered to a broader range of employees in an organization. NSOs are not subject to the same tax treatment as ISOs, and their tax implications can be more complex. NSOs are also not subject to a vesting period, which means that employees can exercise their options immediately.

NSOs let employees buy company shares at a fixed price. When exercised, the difference between the market price and the exercise price is taxed as ordinary income. Later gains or losses from selling the shares are taxed as capital gains or losses.

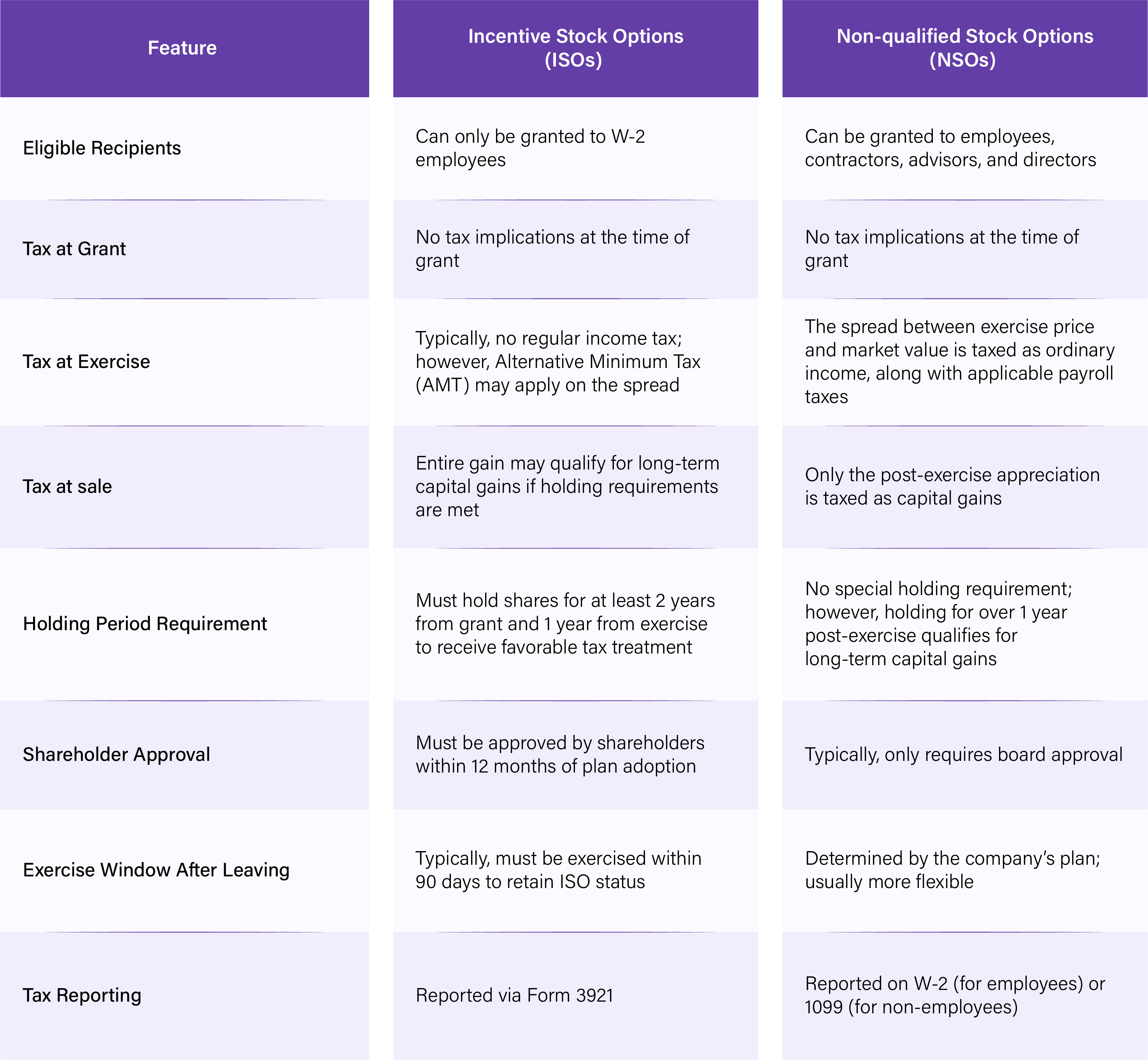

Here are 6 differences between ISOs and NSOs for startups and employees:

1. Tax treatment: ISOs are subject to specific rules and regulations under the Internal Revenue Code, which govern their tax treatment. ISOs are generally taxed at a lower rate than NSOs, and employees may be able to defer taxes on their gains until they sell their shares. NSOs, on the other hand, are subject to ordinary income tax rates, and employees must pay taxes on their gains in the year they exercise their options.

2. Eligibility: ISOs are typically offered to key employees, such as executives and managers, and are designed to incentivize them to work towards the long-term success of the company. To be eligible for ISOs, employees must meet certain requirements, including being employed by the company for a minimum period of time and not owning more than 10% of the company's stock. NSOs, however, are typically offered to a broader range of employees, including contractors, and consultants.

3. Exercise price: The exercise price of ISOs is typically set at the fair market value of the company's stock on the date of grant. NSOs, on the other hand, can be granted at a discount on the fair market value of the company's stock.

4. Vesting period: ISOs are subject to a vesting period, which means that employees must wait a certain amount of time before they can exercise their options. NSOs, on the other hand, are not subject to a vesting period, which means that employees can exercise their options immediately.

5. Transferability: ISOs are generally not transferable, except in limited circumstances. NSOs, on the other hand, can be transferred to other individuals or entities.

6. Alternative minimum tax (AMT): ISOs are subject to the Alternative Minimum Tax (AMT), a separate tax system designed to ensure that high-income taxpayers pay a minimum amount of tax. NSOs do not fall under the Alternative Minimum Tax (AMT) regime.

Here are the differences between ISOs and NSOs.

The answer to this question depends on a variety of factors, including the employee's tax situation, the company's goals, and the employee's long-term plans. ISOs are generally more favorable from a tax perspective, as they are subject to a lower tax rate and may be eligible for tax deferral.

However, ISOs are subject to specific rules and regulations, and not all employees may be eligible for them. NSOs, on the other hand, are more flexible and can be offered to a broader range of employees. Ultimately, the decision of whether to offer ISOs or NSOs will depend on the specific circumstances of the company and its employees.

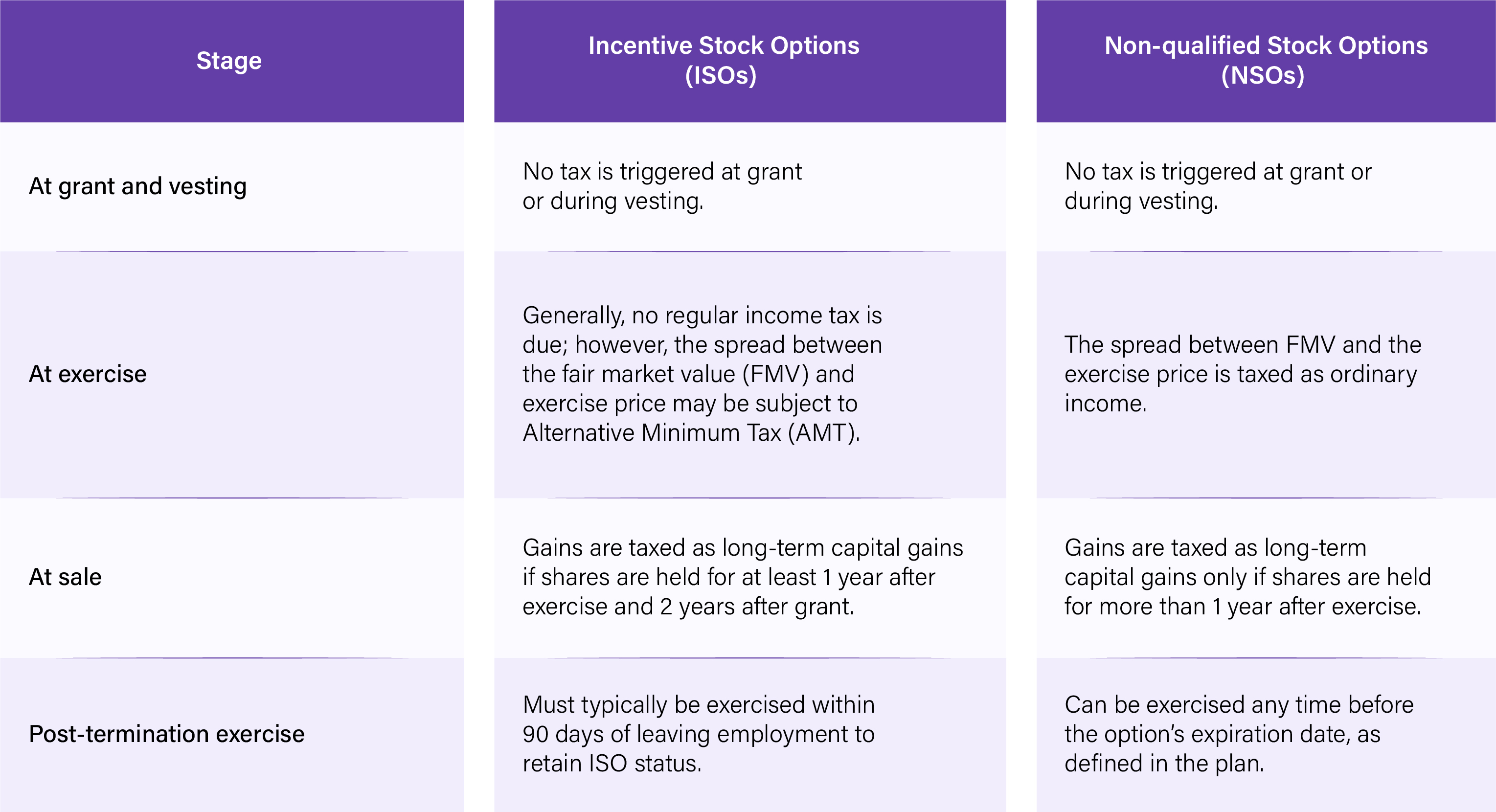

ISOs provide tax benefits if you hold shares for at least 2 years from grant and 1 year from exercise.

However, ISOs come with a key consideration: the Alternative Minimum Tax (AMT). When you exercise ISOs, the difference between the exercise price and the fair market value (FMV) at the time of exercise, the 'spread', is considered income for AMT calculations. This means you may have to pay AMT for that tax year, even though you have not sold the shares or received cash. The AMT is a parallel tax system that can result in a higher tax bill for those who trigger it with incentive stock option exercises.

For instance, if an employee is granted 100,000 ISOs at $2 and exercises them when the FMV is $10, the $800,000 spread may be subject to AMT.

Given these complexities, founders and early employees should monitor vesting, track FMV changes, and assess AMT exposure, especially before major liquidity events. Consulting with a tax professional is highly advisable.

Non-qualified stock options (NSOs) are taxed as ordinary income at the time of exercise. The taxable amount is the difference between the strike price and the fair market value (FMV) of the shares. If you later sell the shares and hold them for more than one year, any additional gain is taxed as long-term capital gains.

For instance, suppose you receive 100,000 NSOs at a $2 strike price. If you exercise them when the FMV is $10, the $ 8-per-share spread results in $800,000 of taxable ordinary income. You must cover this tax either through personal funds or by selling a portion of the shares. Any shares you retain may qualify for long-term capital gains tax upon sale if held for at least one year.

Here are the differences in the tax treatment of ISOs and NSOs at a glance.

In conclusion, ISOs and NSOs are two common types of stock options that companies offer to their employees. While both types of options provide employees with the opportunity to purchase company stock at a discounted price, there are significant differences between the two. Understanding the differences between ISOs and NSOs is essential for employees and startups, as they can have significant implications for tax treatment and potential benefits.

Managing ISOs, NSOs, vesting schedules, and compliance across your option pool is complex. Qapita simplifies it all in one platform. From grant issuance to exercise, we keep your equity program accurate, compliant, and investor-ready.

Book a free demo and see why leading startups trust Qapita for equity management.

ISOs do not automatically convert to NSOs. However, if specific ISO requirements, such as holding periods or employment conditions, are not met, they may lose their ISO status and be treated as NSOs for tax purposes. Companies should clearly outline these conditions in their stock option agreements.

Exercising ISO stock options can be beneficial due to potential tax advantages. However, consider factors like your financial situation, the company's prospects, and potential Alternative Minimum Tax (AMT) implications. Consult with a financial expert to make an informed decision based on your specific circumstances.

ISO (Incentive Stock Option) is a type of employee stock option with potential tax benefits. IPO (Initial Public Offering) is when a company first offers shares to the public. They are unrelated concepts: ISOs are compensation tools, while an IPO is a significant event in a company's lifecycle.

When ISO options expire, the right to purchase company stock at the predetermined price is lost. Unexercised options become worthless, and employees forfeit the opportunity to benefit from potential stock appreciation. It is crucial to be aware of expiration dates and exercise options before they lapse.

Pros of NSOs include flexibility in granting to non-employees and no AMT concerns. Cons include immediate taxation upon exercise and ordinary income tax rates on gains. NSOs offer more flexibility for companies but may be less tax-advantageous for employees compared to ISOs.