Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

As a startup, your company can offer stock options or restricted stock as a part of employee compensation or as a reward for meeting performance goals. However, when employees receive these stock options, they are not immediately eligible for the financial benefits. These stock awards generally follow a vesting schedule that determines how long your employees must wait before they can exercise the options and avail of the financial benefits.

The stock vesting process is crucial for effective financial planning and can significantly impact your company's ability to attract talented individuals. This blog explores different aspects of stock vesting including its meaning, types, working, and impact on your startup's financial strategy. Keep reading to learn more.

Stock vesting is a key concept in employee equity compensation, where employees earn the right to ownership of stock or stock options over a period of time or by meeting specific performance milestones. Vesting ensures that employees remain committed to the company for a certain period or achieve specific performance milestones before they gain full ownership of their equity. This process typically follows a schedule that determines when employees gain full ownership of their equity.

This schedule can be time-based, where ownership rights are granted incrementally over a set period, or performance-based, where specific targets must be met. For example, a common vesting period is '4-year vesting with a 1-year cliff,' meaning the employee must stay with the company for at least one year before any stock options vest, and thereafter, they vest gradually over the next three years.

Different types of stock options, such as Incentive Stock Options (ISOs), Non-Qualified Stock Options (NSOs), and Restricted Stock Units (RSUs), can be subject to vesting. Understanding their tax implications and exercise requirements can help create a balanced stock vesting schedule that aligns with your company's long-term goals.

Incentive Stock Options (ISOs) are a type of stock option that allows employees to purchase company shares at a pre-determined price. The vesting process for ISOs usually involves a time-based schedule, where a certain percentage of the options vest each year. For example, an employee might have 25% of their ISOs vest each year over a four-year period. This ensures that employees remain with the company for a longer duration to gain full ownership of their options.

One key aspect of ISOs is their favorable tax treatment. When employees exercise their ISOs, they do not have to pay taxes immediately. Instead, they may qualify for long-term capital gains tax rates if they hold the shares for at least one year after exercising and two years after the grant date. However, it is important to note that exercising ISOs may lead to the Alternative Minimum Tax (AMT), which can have a significant impact on the timing of exercising these options.

Non-Qualified Stock Options (NSOs) are another type of stock option that companies can offer to employees. Unlike ISOs, NSOs do not qualify for special tax treatment, which means they are subject to different tax rules.

NSOs typically follow a similar vesting schedule as ISOs, where employees earn the right to exercise their options over a set period. This can be a time-based schedule or tied to specific performance milestones. Once the NSOs vest, employees can choose to exercise their options, but they are not required to do so immediately.

The primary difference between NSOs and ISOs lies in their tax treatment. When employees exercise their NSOs, they are required to pay taxes on the gap between the pre-determined exercise price and the Fair Market Value (FMV) of the shares. This amount is considered ordinary income and is subject to income tax. Additionally, when employees sell the shares, they may be subject to capital gains tax on any further appreciation.

Restricted Stock Units (RSUs) are another type of equity compensation but are different from stock options. RSUs represent a promise to deliver shares of company stock to employees once certain conditions are met. As a startup founder, it's important to understand how RSUs vest and the implications for your equity compensation plans.

RSUs typically vest over a certain amount of time, following a pre-determined schedule. This can be based on the employee's tenure with the company or specific performance milestones. Once the RSUs vest, the shares are automatically delivered to the employee, and they gain full ownership of the stock.

One key difference between RSUs and stock options is that RSUs always have some value, as they represent actual shares of stock. When RSUs vest, the FMV of the shares is considered ordinary income, and a portion of the shares is withheld to cover income taxes. Employees can then choose to hold or sell the remaining shares.

Here are the different steps involved in the stock vesting process:

1. Stock Option Grant: On the grant date, the company awards the employee stock options or restricted stock units (RSUs). The number of shares granted and the vesting schedule are determined at this time.

2. Stock Option Vesting: This is the timeframe during which the employee gradually earns the right to exercise their options or receive their shares. Vesting can be linear or in stages, with a specific percentage of shares vesting at regular intervals.

3. Meeting Vesting Conditions: These are the conditions that employees must meet to earn the vested shares. The most common condition is continued employment with the company. Some companies may also include performance-based vesting conditions.

4. Stock Option Exercise: In the case of stock options, the exercise date is the day when employees can choose to exercise their options and purchase the underlying shares at the pre-determined strike price. They must pay the exercise price, which is typically a discounted rate compared to the market price. In the case of RSUs, shares are delivered on vesting and there is no concept of exercise.

5. Owning Vested Shares: Once the exercise process is complete in the case of options or once vesting is completed in the case of RSUs, the employee owns the vested shares. They can then sell the shares on the open market or hold onto them for potential future gains.

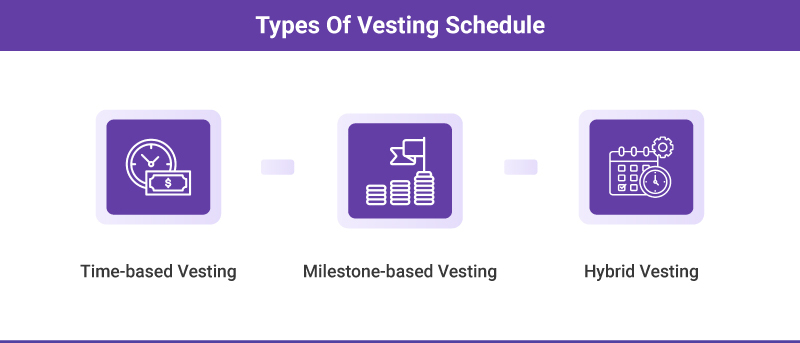

A vesting schedule specifies a timeline that determines when employees gain ownership of their stock options or shares. Vesting schedules ensure that your employees remain committed to the company for a certain period or achieve specific performance milestones before they gain full ownership of their equity.

The significance of a vesting schedule lies in its ability to incentivize employees to continue working with the company and contribute to its long-term success. By implementing a well-structured vesting schedule, you can ensure that your employees are rewarded appropriately and remain motivated to help your company achieve its objectives.

Time-based vesting is a common method in which employees earn stock options or shares over a set period. A typical time-based vesting schedule is a four-year plan with a one-year cliff. In this schedule, employees must stay with your company for at least one year before any of their equity vests.

After the first year, a portion of the equity vests, and the remaining equity vests gradually over the next three years. For example, an employee might have 25% of their stock options vest after the first year and the remaining 75% vest in equal monthly or quarterly installments over the next three years.

This method benefits both you and your employees. For you, it ensures that employees are committed to the company for a longer period, reducing turnover and retaining valuable talent. For the employee, it provides a clear timeline for gaining ownership of their equity, offering a sense of security and motivation to contribute to the company's success.

Milestone-based vesting is a type of vesting schedule where stock options or shares vest based on the achievement of specific performance milestones. This type of vesting encourages employees to work towards key company goals, ensuring that their efforts directly contribute to the company's success.

Typical milestones for milestone-based vesting can include:

1. Company IPO: Employees' stock options or shares vest when the company goes public.

2. Revenue Targets: Vesting occurs when the company reaches specific revenue milestones.

3. Product Launches: Employees earn their equity upon the successful launch of a new product or service.

4. Funding Rounds: Vesting is tied to the completion of significant funding rounds.

By tying vesting to these milestones, you create a strong incentive for employees to meet objectives that are critical to your company's growth and success. This approach ensures that their interests are aligned with those of the company.

Hybrid vesting schedules combine elements of time-based and milestone-based vesting. This approach offers flexibility and can be customized to satisfy your company's particular needs. Hybrid vesting allows you to create a balanced vesting schedule that rewards employees for their tenure and their contributions to achieving key milestones.

For example, a hybrid vesting schedule might include:

1. Time-Based Component: A portion of the stock options or shares vest over a set period, such as 50% vesting over four years with a one-year cliff.

2. Milestone-Based Component: The remaining 50% vests upon the achievement of specific milestones, such as reaching a revenue target or completing a product launch.

This combination ensures that employees are incentivized to stay with the company for a longer duration while also working towards critical company goals.

Graded vesting is a method by which employees gradually earn ownership of their stock options or shares over a specified period. Unlike cliff vesting, where employees gain full ownership of their equity all at once after meeting a specific requirement, graded vesting allows employees to vest in increments. This approach ensures that employees earn a higher percentage of their benefits as their tenure with the company increases.

For example, a typical graded vesting schedule might involve 20% vesting per year over five years. In this scenario, an employee would earn 20% of their stock options or shares after the first year, 40% after the second year, and so on until they are fully vested at the end of the fifth year. This gradual accumulation of ownership rights provides employees with a sense of progress and motivation to stay with the company.

You might prefer graded vesting for several reasons. First, it encourages employee retention by incentivizing your employees to remain with the company for a longer duration. Second, graded vesting promotes long-term commitment and loyalty as your employees see their benefits grow over time. Finally, it offers flexibility, allowing employees who leave your company before becoming fully vested to still claim a portion of their benefits based on the amount they have already vested.

Cliff vesting is another type of vesting schedule where employees must meet a specific requirement, such as staying with the company for a certain period, before any of their stock options or shares vest. This approach ensures that employees are committed to the company for a minimum duration before they gain any ownership of their equity.

For example, a common cliff vesting schedule is a one-year cliff followed by monthly or quarterly vesting. In this scenario, employees must remain with the company for at least one year before any of their stock options or shares vest. After the initial one-year cliff, the remaining equity vests gradually over the subsequent months or quarters.

A one-year vesting cliff is a specific type of cliff vesting in which employees must remain with the company for at least one year before any of their stock options or shares vest. Startups commonly use this approach to ensure that employees are committed to the company for a significant period before they gain ownership of their equity.

The strategic purpose of a one-year cliff is to encourage employee retention and reduce turnover. By requiring employees to stay with the company for at least one year before any of their equity vests, your company can retain the best employees and reduce the costs associated with high turnover rates. A one-year cliff also provides employees with a clear timeline for gaining ownership of their equity, offering a sense of security and motivation to stay with the company.

For employees who leave the company before the one-year cliff date, none of their stock options or shares will vest. This means that they will not gain any ownership of their equity if they do not meet the initial vesting requirement.

When an employee leaves the company before their stock options are fully vested, they typically forfeit the unvested portion of their equity. This process is known as forfeiture, which implies that the unvested stock options or shares are returned to the company, and the employee loses the right to own them.

The concept of forfeiture is designed to ensure that employees remain committed to the company for a certain period or achieve specific performance milestones before gaining full ownership of their equity. For example, if an employee has a four-year vesting schedule and leaves the company after two years, they would forfeit the remaining unvested stock options or shares.

There are some exceptions where employees might hold-on to the unvested awards. These exceptions typically occur under specific circumstances, such as:

1. Retirement: Some companies have provisions that allow employees to retain unvested awards if they retire after meeting certain criteria, such as age and years of service.

2. Termination without cause: In some cases, if an employee is terminated without cause, they may be allowed to retain a portion of their unvested awards or have them accelerated to vest immediately.

3. Change of control: If the company undergoes a significant event, such as an acquisition or merger, unvested awards may be accelerated to vest immediately.

As a startup founder, you must have a clear grasp of concepts like vesting schedules and the different types of stock vesting. This helps ensure that you can design effective compensation plans that align with your company's goals and motivate your employees. Whether it's time-based, milestone-based, or hybrid vesting, each approach has its unique benefits and implications for your company and your employees.

At Qapita, we specialize in helping companies manage their equity and vesting schedules efficiently. Our comprehensive equity management platform is rated as #1 in the category by G2. It allows you to easily manage all aspects of your company's equity, from cap table management to ESOP issuance and valuation for accounting and tax compliance. We provide a one-stop solution for all your equity management needs, ensuring that your employees are engaged and motivated.

If you need personalized advice on managing your company's equity and vesting schedules, we are here to help. Contact us today to learn more about how our experts can support your company's growth and success.