Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

Startups are known for their innovative and fast-paced culture that offer multiple exciting growth opportunities for employees. While new challenges and dynamic environments continue to attract fresh talent, it often becomes difficult for startups to retain employees for the long haul. In such a scenario, stock options prove to be a powerful tool that creates a sense of ownership in employees and aligns their objectives with company goals.

Among various equity compensation options available, Non-Qualified Stock Options (NSOs) are a popular choice. Unlike Incentive Stock Options (ISOs), NSOs don't offer any immediate tax advantages, but they provide excellent flexibility when structuring compensation packages.

This blog covers different aspects of NSOs, including their working, taxation, advantages, challenges, and others. Let us dive in.

Non-Qualified Stock Options (NSOs) are a form of employee compensation that provides the holder the right, but not the obligation, to buy a certain number of shares of the company stock at a fixed price (exercise or strike price). This contract is typically valid for a specified period, known as the vesting period, after which it expires. Unlike ISOs, companies can offer NSOs to anyone, including employees, consultants, advisors, and board members, providing you with greater flexibility in distributing equity.

NSOs are called 'non-qualified' as they do not satisfy the conditions defined by the Internal Revenue Service (IRS) to be classified as Incentive Stock Options (ISOs) that are eligible for special tax treatment. When an NSO is exercised, the spread between the present Fair Market Value (FMV) of the stock and its strike price is regarded as ordinary income, subject to income tax withholding. This income is reported on the employee's tax return.

The tax treatment of Non Qualified Stock Options is different from that of Incentive Stock Options (ISOs), which are typically not taxed at exercise but may be subject to the Alternative Minimum Tax (AMT).

When employees use their NSOs, the difference between the purchase price and the current FMV of the stock is subject to federal income tax, which can vary from 10% to 37%. This difference is also subject to state income tax (if it applies), as well as payroll taxes like Medicare and Social Security.

This ordinary income is reported on the employee's W2 form. This means that the tax obligation arises at the time of option exercise, regardless of whether the employee decides to sell the shares or hold onto them.

After exercising the options, when employees sell the stock, any extra profit or loss is regarded as a capital gain or loss. The nature of this gain or loss depends on how long the stock was held after exercise.

If the stock is held for more than a year, it is eligible for long-term capital gains tax rate (varying between 0% to 20%), which are generally lesser than the ordinary income tax rate. This can be a major advantage for employees who wish to retain their shares for a longer period.

The lifecycle of NSOs can be broken down into several key phases: Grant, Vesting, Exercise, Taxation, and Tracking. Each phase has its own set of rules and implications that are important for you to understand.

The journey of Non Qualified Stock Options begins with the grant phase. This is when you, as an employer, offer stock options to your employees. The grant includes the following key elements:

The terms of the grant, clearly defined at this stage, can include details about the vesting schedule, option expiration date, and any restrictions on the sale of the stock after exercise.

The next phase is vesting, which determines when your employees can exercise their options. Vesting schedules can vary, but the most common option is a 4-year vesting schedule, where each year, 25% of the total grant of NSOs becomes available for your employees to exercise. Other types of vesting schedules include cliff vesting (100% of the NSOs will be vested at the same time after a certain period) and graded vesting (the NSOs will be vested gradually, e.g., 25% per year and vested in four years).

The exercise phase is when your employees decide to purchase the company's common stock at the grant price. They can opt to pay the exercise price in cash, or if you allow it, they can opt for a cashless exercise or sell to cover. In a cashless exercise, your employees sell a portion of their shares to cover the exercise cost, whereas, in a sell-to-cover, they sell shares immediately to cover the exercise price and taxes.

The taxation phase is critical to understand as it has significant financial implications for your employees. Exercising NSOs triggers tax implications for employees as it creates a reportable income subject to federal and state taxes. The taxable amount is calculated as follows:

Taxable amount = Number of Shares Exercised * (Market Value at Exercise - Grant Price)

This income is reported on the employee's tax return. It is included in their overall compensation income and is reflected on Form W-2 (Form 1099 for non-employee participants)

Tracking Non Qualified Stock Options is important for both you and your employees. It ensures compliance with IRS guidelines and efficient management of the stock options throughout their lifecycle. There are various tools and services available for managing and tracking the lifecycle of stock options. These tools can provide real-time updates, automate calculations, generate reports, and even offer predictive analytics to help your employees make informed decisions.

Deciding when to exercise Non Qualified Stock Options can be a complex process for your employees. This decision is not just about the numbers on a spreadsheet but also about their personal financial goals, the performance of your company, and the current market conditions. Here are some factors that they should consider:

For better understanding, let's consider a scenario where an employee of your rapidly growing tech startup holds Non Qualified Stock Options with an exercise price of $15 per share. The present market price is $40 per share. Your company has demonstrated strong financial health and promising future growth. The employee expects a lower income this year due to a career break. Given these factors, exercising the options this year might be advantageous. The employee can lock in a profit of $25 per share, benefit from favorable tax treatment by holding the stock for over a year and align with their long-term financial goals.

Here is a detailed analysis of the different benefits and challenges presented by Non Qualified Stock Options.

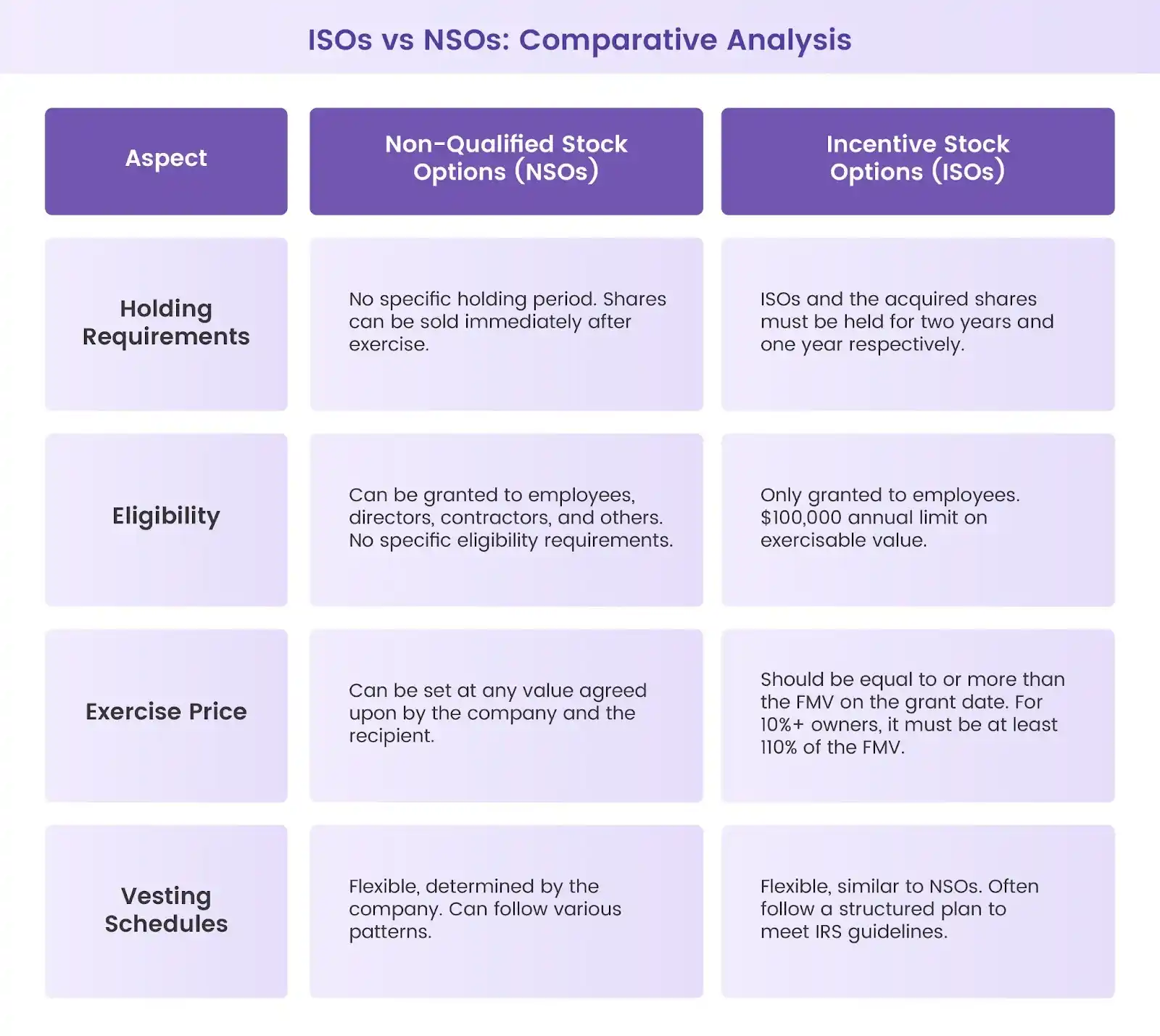

When considering stock options as part of your employee compensation plan, it is crucial to understand the differences between NSOs and ISOs. Here is a comparative analysis for these two main types of stock options:

Understanding NSOs is crucial for you as a startup founder as it helps you attract and retain top talent and also align your team's interests with the company's success. However, managing NSOs can be complex, especially when it comes to important aspects like taxation and tracking. That's where we, at Qapita, come in. As a leading equity management platform, we are committed to unlocking the power of ownership for startups and have over 2,000 companies and 300,000 employee-owners as our partners.

Our platform is rated as #1 in the equity management software category by G2 and can easily manage all equity matters for your company from inception to IPO. But our support doesn't stop at providing a platform. We understand that every startup has unique needs and challenges. That is why we offer one-on-one consultation services from our in-house experts in equity management, who are ready to guide you through the crucial aspects of equity management.

Whether you need help with plan review, employee education, or understanding the nuances of your equity scheme, we are here to assist. Reach out to our experts for more information on our services.

While complete tax avoidance is not possible, you can minimize taxes on NSOs. Consider exercising when the stock price is low to reduce the taxable spread. Holding shares for at least a year after exercise may qualify you for long-term capital gains rates on future appreciation. Strategic timing of exercises across tax years can also help manage your overall tax liability.

Restricted Stock Units (RSUs) represent shares granted to employees, while non-qualified stock options (NSOs) provide the right to buy shares at a set price. RSUs are taxed when vested, while NSOs incur taxes at exercise and sale, making NSOs more flexible but with potential higher tax exposure.

An example of a non-qualified stock option is when a company grants an employee the right to buy 1,000 shares at $10 each. If the stock price rises to $20, the employee can exercise the options, pay $10,000, and potentially sell the shares for $20,000, incurring tax on the $10,000 gain.

NSOs are not taxed twice but have two potential tax events. First, when exercised, the difference between the exercise price and fair market value is taxed as ordinary income. Second, if the stock is later sold at a higher price, the additional gain is taxed as a capital gain. This ensures both compensation and investment gains are appropriately taxed.

To minimize taxes on NSOs:

1. Exercise when the stock price is low to reduce the taxable spread.

2. Consider a cashless exercise to cover exercise costs and taxes.

3. Hold shares for at least a year after exercise for potential long-term capital gains treatment.

4. Time exercises strategically across tax years to manage your overall tax liability.