Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

.jpg)

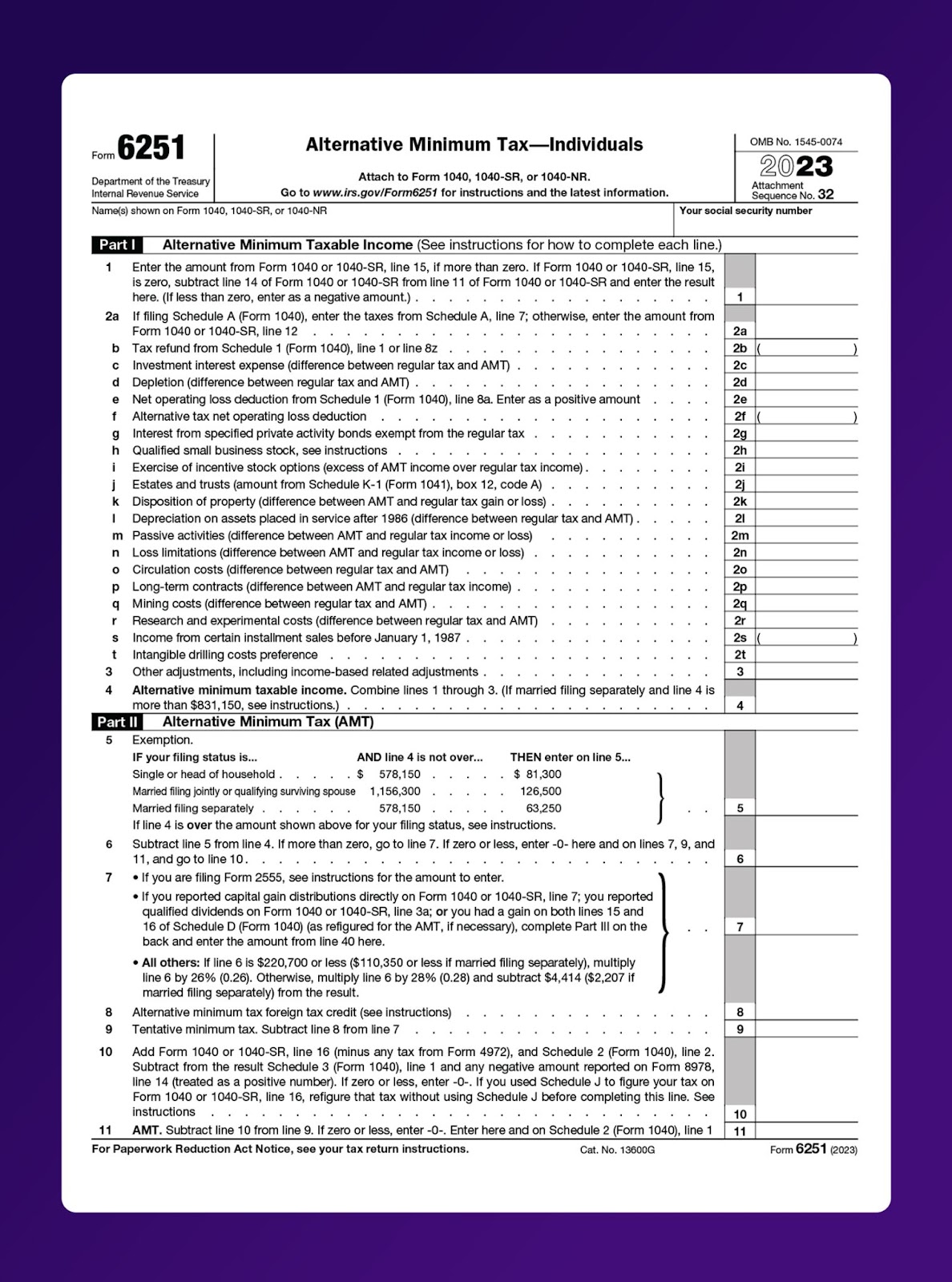

Navigating the complexities of tax preparation as per current regulations is an important aspect of running a startup. As a founder, understanding these regulations can significantly impact your business's financial health. One key tax form you need to be familiar with is Form 6251, which is vital for determining the Alternative Minimum Tax (AMT) that you may owe.

This form can have a direct impact on your financials, especially if you are dealing with stock options or any other form of equity compensation. In this blog, we will cover the different facets of Form 6251, including its purpose, filing dates, important sections, and how it relates to AMT. Keep reading to learn more.

The AMT is a separate tax system in the US designed to ensure that certain individuals, particularly those with higher incomes, pay a fair share of taxes. The AMT operates alongside the standard tax system and has its own set of rules and rates implemented by the United States federal government.

Essentially, taxpayers with relatively high incomes are required to compute their income tax twice: once under the standard tax rules and once under the AMT rules. They then are expected to pay the larger amount of the two calculations. The AMT aims to prevent taxpayers from significantly reducing their tax liability through certain deductions or tax breaks.

Prior to the AMT, some high-income earners legally paid minimal taxes due to how certain income and expenses were treated. The AMT addresses this by recalculating income tax after adding specific tax preference items to the adjusted gross income. This ensures that even with deductions, taxpayers contribute a minimum amount in taxes.

Multiple factors can affect AMT calculation, impacting whether you are subject to this tax and the amount you may owe. Here are the factors reported on Form 6251 and how they play a crucial role in determining your overall tax liability.

1. Income Level: Your income level can significantly influence whether you are subject to the AMT. If your income exceeds certain thresholds (specified above), you may need to calculate your tax liability under the AMT as well as the regular tax system. Then, you are required to pay the higher of the two amounts as tax.

2. Filing Status: Your filing status (e.g., single, married, filing jointly, head of household, etc.) can also affect the calculation of the AMT. The IRS sets different exemption amounts for each filing status, and this information is readily available on Form 6251.

3. Deductions: Certain deductions you claim on your regular tax return may not be allowed or might be limited for AMT purposes. This can include deductions for state and local income taxes, interest on home equity loans used for non-improvement purposes, and certain depreciation methods. Form 6251 has specific sections for reporting these adjustments. Remember, claiming deductions that reduce your regular tax liability might inadvertently push you into AMT territory.

4. Type of Income: Certain types of income, such as interest income from specific private activity municipal bonds, can make you subject to the AMT. These income types are added back to your taxable income when calculating the AMT, increasing your tax liability.

Incentive stock options (ISOs) can be a powerful tool for motivating your team by giving them a stake in the company's success. However, exercising ISOs can also trigger an unexpected tax liability in the form of AMT.

IRS Form 6251, officially known as the Alternative Minimum Tax Individuals, is a tax document utilized by the Internal Revenue Service (IRS) to calculate the potential AMT that a taxpayer might owe. This form comes into play when taxpayers with substantial incomes leverage certain deductions to decrease their tax bill.

The AMT operates as a safeguard, establishing a ceiling on these tax benefits to make sure that individuals with higher incomes contribute a fair share of taxes. It acts as a balancing mechanism in the tax system, preventing excessive deductions and ensuring tax equity. Hence, if you fall into the taxpayer category for which the AMT is applicable, your tax obligation will be determined by the AMT instead of the standard deduction in the individual tax return.

The requirement to file Form 6251 depends on specific income thresholds and other criteria. For the tax year 2024, the Internal Revenue Services (IRS) has set the following guidelines for the Alternative Minimum Tax (AMT):

In addition to the income thresholds discussed here, there are specific conditions under which you must attach Form 6251 to your tax return. These conditions include:

Filing deadlines can be stressful, especially for busy startup founders like you. However, when it comes to Form 6251, knowing the key dates can save you time and potential penalties. Here is a breakdown of these dates for 2025 to ensure you meet the filing requirements:

You must complete the filing deadline to avoid a late filing penalty. This penalty is usually 5% of the tax owed for every month or part of the month for which your return is late, but it can go up to a maximum of 25%.

Each section of Form 6251 is integral to determining whether you owe the AMT and, if so, how much. Let's break down the key sections and what information they require.

AMT calculation involves a series of steps using Form 6251. Here's a step-by-step guide to help you navigate this process:

Filing Form 6251 with the IRS involves several steps. Here is a breakdown of the entire process:

1. Gather Necessary Documents: Before you start, make sure you have all the necessary documents. This includes W-2s, 1099s, and any other forms reporting your income.

2. Download Form 6251: You can download the Form 6251 PDF on your desktop or laptop directly from the IRS website. To avoid any issues, ensure you have the recent version of the form.

3. Complete the Form:

4. Double-Check Your Information: Ensure all entries are accurate. Errors can lead to delays, additional scrutiny from the IRS, and potential penalties.

5. Submit Your Form: Attach Form 6251 to your regular tax return (Form 1040) and submit it to the IRS. You can file electronically or mail a paper return.

6. Pay Any Due Tax: If the AMT results in additional tax liability, ensure you make the payment by the tax filing deadline.

Form 1040 is the primary tax return form for individuals in the United States. It encompasses all your income, deductions, credits, and tax payments to determine your regular tax liability. However, the tax code requires certain high-income earners to calculate their taxes under the AMT system, which is where Form 6251 comes into play.

Let's explore the connection between both these forms:

1. Calculating Alternative Minimum Taxable Income (AMTI): When you complete Form 1040, you calculate your taxable income based on regular tax rules. Form 6251 then requires adjustments to this income to determine your AMTI. These adjustments can include adding back certain deductions and income that are not allowed under AMT rules.

2. Determining AMT Liability: After calculating your AMTI on Form 6251, you compute your tentative minimum tax. If this amount is higher than your regular tax liability calculated on Form 1040, the difference is your AMT liability. This ensures that you pay the greater of your regular tax or the AMT.

3. Reporting AMT on Form 1040: Once you determine your AMT liability using Form 6251, you report this amount on Form 1040, specifically on line 46. This ensures that your total tax liability reflects the higher amount between your regular tax and AMT.

Errors in either form can lead to incorrect tax calculations, resulting in overpayment or underpayment of taxes. Overpayment ties up your capital unnecessarily, while underpayment can lead to penalties and interest charges.

Understanding Form 6251 and AMT is crucial, especially for startup founders dealing with equity compensation. The complexities of these tax matters can be daunting, and professional advice is often necessary.

At Qapita, we recognize these challenges. Our Equity Management Software is rated as #1 by G2 and is optimized to simplify the equity matters for your company. We offer a comprehensive solution for managing ownership, streamlining equity workflows, and providing a structured marketplace for liquidity. Trusted by over 2,400+ companies and 300,000 employee-owners, we aim to make every equity owner count.

Whether you're grappling with Employee Stock Ownership Plans (ESOPs), capitalization tables (CapTables), or tax-related matters like the AMT, Qapita is here to help. Our in-house experts can provide the guidance and support you need. Contact us today to learn more.