Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

As a startup founder, you likely offer stock options to attract and retain talent, but have you considered what happens to those options when an employee leaves your company? This is where the Post Termination Exercise Period (PTEP) comes into play. It refers to the time frame an employee has to exercise their vested stock options after leaving your company.

Understanding this period is essential for your team members because it directly impacts their financial decisions and potential returns from equity compensation. For employees, the PTEP can be a golden opportunity to secure financial gains, but it also poses challenges like tight deadlines and unexpected tax implications. Knowing how this period works helps them plan better, avoid costly mistakes, and maximize the value of their hard-earned equity.

This blog covers the core aspects of the post termination exercise period, providing insights that help you make well-informed decisions in this complex area.

The Post-Termination Exercise Period (PTEP) defines the time period your former employees have to purchase their vested stock options after leaving your company. Typically, this window ranges from 90 days to as long as 10 years, depending on your company's equity plan.

The PTEP forces critical financial decisions for employees. They must decide whether to buy shares, often requiring significant cash, or let the options expire, losing potential gains.

For example, an employee leaves your startup after four years with fully vested options. If your PTEP is 90 days, they have just three months to come up with the cash to exercise their options. This can be a significant financial burden, especially if your company's valuation has increased substantially. On the other hand, a longer PTEP of several years gives them more time to make an informed decision and potentially secure the necessary funds.

The standard 90-day PTEP has its roots in IRS regulations, specifically Section 422 of the Internal Revenue Code, which requires exercise within three months of termination to maintain tax benefits. Historically, this short window aimed to encourage quick decisions while aligning with tax rules. Over a period of time, however, economic shifts and employee advocacy have driven change.

In recent years, there has been a shift towards extended PTEPs, particularly among tech startups driven by several factors:

While the 90-day PTEP remains common, particularly for Incentive Stock Options (ISO), there is significant variation across the startup ecosystem.

Here is how the post-termination exercise period is significant for your employees and your startup's equity strategy.

When your employees fail to exercise their options within the set PTEP, the consequences can be severe:

Let's look at a quick example for clarity:

An employee leaves your company with 10,000 vested options at a strike price of $1 per share. Your company's current fair market value is $10 per share. If the employee fails to exercise within the PTEP:

This $90,000 represents the immediate paper gain the employee would forfeit. If your company continues to grow and eventually goes public or gets acquired at a higher valuation, the lost opportunity could be even more substantial.

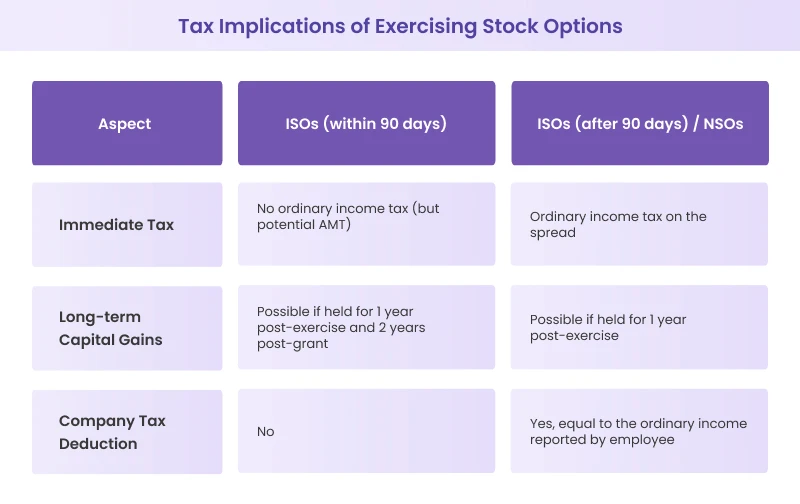

The tax consequences of exercising stock options can be complex and vary depending on the type of options and when they are exercised. Here is a breakdown of the key considerations:

Here is a simplified comparison table:

Exercising options, especially for a private company, can create a significant tax burden without providing liquid assets to cover the taxes. This is often referred to as the 'golden handcuffs' problem.

For your employees, the decision of when to exercise involves balancing potential tax benefits against the risk of investing in illiquid stock. As a founder, you should encourage them to seek professional advice from a financial advisor or subject-matter expert to understand their specific situation.

Navigating the post termination exercise period often presents hurdles for your employees, impacting their ability to benefit from stock options. These challenges stem from tight deadlines, financial burdens, and unclear contract terms. Let's analyze these challenges further.

Most companies set a 90-day post termination exercise period for incentive stock options due to IRS requirements, but this brief window can pressure your employees into hasty decisions. Within three months, they must decide whether to exercise their options, often needing substantial funds while adjusting to new financial realities after leaving your company.

If they miss this deadline, their options expire, potentially costing them significant gains. In contrast, companies offering extended windows, like seven or 10 years, give employees more breathing room to evaluate market conditions and secure funds.

A longer post-termination exercise period reduces risk and fosters goodwill, encouraging your team to view equity as a long-term benefit rather than a rushed obligation.

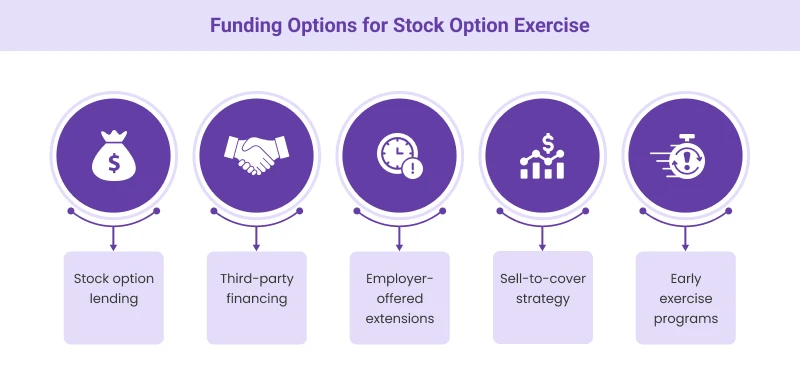

The financial burden of exercising stock options is often a significant hurdle for employees.

If they lack savings, funding this exercise becomes a challenge. Some employees turn to specialized firms offering loans tailored for option exercises, allowing them to cover costs without upfront cash. Others might sell personal assets or tap into retirement savings, both of which carry risks.

Many employees don't fully grasp their stock option agreements, leading to missed opportunities during the post termination exercise period. They might skim over critical details like exercise deadlines, assuming they have more time than they do. Others overlook tax obligations, leaving them unprepared for liabilities at exercise or sale.

Company buyback policies also catch some off guard, if your startup reserves the right to repurchase shares, employees need to know the terms to avoid surprises. Encourage your team to review their contracts carefully, focusing on the exercise window, vesting schedule, and any clauses about early termination.

Providing educational resources or access to advisors can bridge this knowledge gap, ensuring they approach their options with confidence and clarity.

Here is how you can ensure that your team members make informed decisions about their stock options, even after they leave your company.

Encourage your employees to thoroughly review their equity agreements before resigning. This proactive approach can prevent misunderstandings and potential financial losses. These are key areas they should focus on:

Many employees struggle with the financial burden of exercising their options after leaving. As a founder, you can provide information about various financing methods:

Your employees might have room to negotiate a longer post-termination exercise period before they leave, especially if they have been key contributors. Some companies grant extensions to valued team members, stretching the standard 90-day window to several years as part of a flexible exit package.

For example, a senior engineer might secure a two-year extension by highlighting their role in a critical project. Advise them to build a strong case, referencing industry trends where startups offer extended periods to stay competitive.

They should approach the conversation professionally, emphasizing mutual benefits, like maintaining a positive relationship with your company. Timing matters, so, suggest they start this discussion early, before submitting their resignation, to maximize leverage.

Understanding the post-termination exercise period is vital for your employees and the overall health of your startup's equity strategy. This period dictates how long your team members have to act on their vested stock options after leaving, impacting their financial outcomes and your company's reputation as an employer. Proactive planning can prevent missed opportunities, reduce stress, and ensure fair treatment for departing employees.

At Qapita, we have helped over 2,400 companies and 350,000 employee owners navigate the complexities of equity management. Our equity management platform, rated as #1 by G2, offers comprehensive solutions for CapTable management, ESOP administration, and digital ESOP issuance. We understand the unique challenges you face as a startup founder, and we are here to support you every step of the way.

Book a 1:1 demo with our experts to unlock the full potential of your equity compensation strategy.