Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

As a startup founder operating your company as an LLC, understanding how to distribute business profits is crucial for managing your business finances effectively. LLC distributions are the primary mechanism for you and your co-founders to receive a share of the company's earnings according to every member's interest.

Unlike a traditional salary, which represents compensation for services rendered, distributions are a return on your LLC interest in the business. Understanding how LLC distributions work and how they are taxed is crucial for effective financial planning and compliance. Without this knowledge, you might face unexpected tax liabilities or miss out on opportunities for efficient profit allocation.

This guide will walk you through the fundamental aspects of LLC distributions and their tax implications, providing you with the clarity necessary to manage your startup's finances effectively across each tax year.

LLC distributions are payments made to members of an LLC from the company's profits or capital. These distributions represent each member's share of the company's earnings, based on their ownership percentage or the terms outlined in the LLC's operating agreement.

Unlike salaries, which are regular payments made for services rendered, distributions are typically discretionary and can be made at irregular intervals. This flexibility allows LLCs to adapt to changing business conditions and cash flow needs. For example, if your LLC generates $100,000 in profit and you are the sole member, you could choose to take the entire amount as a distribution. However, if you have multiple members, the distribution would be split according to ownership percentages or the agreed-upon terms.

LLC members primarily receive distributions, not salaries. These distributions are exempt from payroll taxes, such as Social Security and Medicare. However, distributions that are guaranteed payments made regardless of profitability for active participation are considered ordinary income and are subject to self-employment tax.

LLCs are typically pass-through entities for federal income tax purposes. This means the LLC itself is not taxed; instead, profits and losses are passed to members, who report them on their individual tax returns. This structure simplifies tax reporting and allows for direct taxation of earnings at the member level.

As a startup founder, knowing different types of LLC distributions helps you manage profits effectively and simplifies tax planning.

Regular LLC distributions involve sharing profits with members on a routine basis, based on their ownership percentage or another agreed-upon formula. You may use regular distributions as consistent compensation throughout the year, typically on a monthly or quarterly basis. These payments are subject to income tax on your personal return. Planning regular distributions helps you forecast personal income and manage estimated tax payments more accurately.

Special LLC distributions occur when your business experiences unexpected profits or needs to distribute surplus cash outside the regular schedule. For instance, you may approve a special distribution after a particularly profitable quarter or the sale of a significant asset. Like regular distributions, these also pass through to your personal tax return. However, special distributions can influence your overall tax strategy by unexpectedly increasing your annual taxable income.

Liquidating distributions take place when you dissolve your LLC and distribute the remaining assets to the members. These distributions represent a return of your investment rather than regular income. You will calculate the gain or loss based on your initial investment versus the asset's market value at the time of dissolution. Liquidating distributions may receive capital gains tax treatment, potentially reducing your tax liability compared to regular income taxation.

To distribute LLC profits effectively, you must follow these steps:

1. Calculate your company's net earnings after covering all expenses and setting aside reserves.

2. Review your LLC's operating agreement, which specifies how these profits should be allocated as per the membership interest.

3. Following these guidelines, LLC members formally approve the current distribution through a vote or resolution.

4. Finally, funds are transferred from the LLC bank account directly into each distributee member's personal account.

For example, consider a scenario where your new LLC has approved a $10,000 profit distribution. If you and your partner own 60% and 40%, respectively, you receive $6,000, while your partner receives $4,000 in direct proportion to your ownership percentages.

LLC operating agreement serves as the primary roadmap for distributions of profit. It can override default state rules and set custom terms for how and when distributions occur. Key elements to include in this document are:

1. Time of the distribution (e.g., quarterly, annually, or as needed)

2. Method for calculating each member's share

3. Special rules or any restrictions on cash distributions

4. Procedures for approving distributions

Regularly reviewing and updating this document protects your LLC's stability and clarifies each LLC owner's expectations regarding profit distributions. The operating agreement should also address provisions related to the termination of the LLC and liquidation of a member's interests.

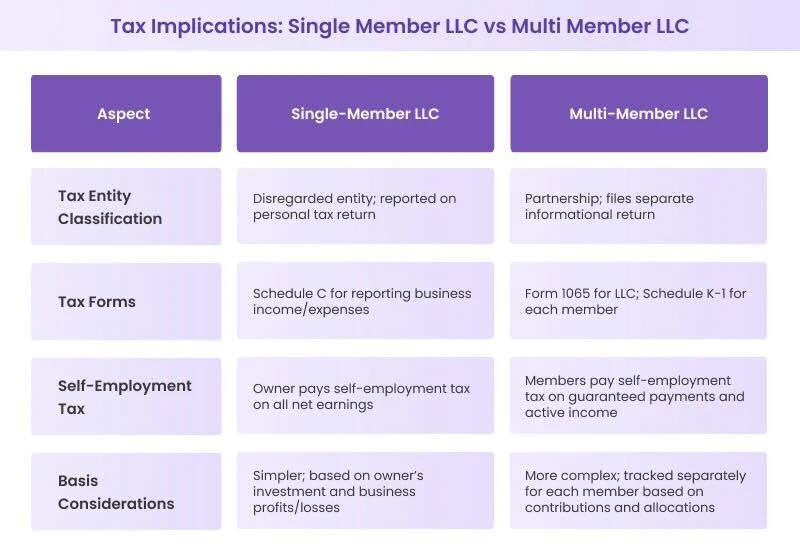

The distribution process varies depending on whether you have a single-member or multi-member LLC. Here is a comparative analysis of both these scenarios:

1. Single-member LLC: You have sole discretion over distribution decisions.

2. Multi-member LLC: Distributions typically require agreement among members, often based on the terms outlined in the operating agreement.

1. Single-member LLC: All profits are allocated to you as the sole owner.

2. Multi-member LLC: Profits are usually distributed based on ownership percentages or as specified in the operating agreement.

1. Single-member LLC: For federal income tax purposes, distributions must be reported on your personal tax return (Schedule C).

2. Multi-member LLC: Each member receives a Schedule K-1 form, which reports their share of the LLC income, which they then report on their individual tax returns.

Here is a brief overview of the tax implications of LLC distributions to help you make informed decisions:

Pass-through taxation is a key benefit of LLCs. Your business profits flow directly to your personal tax return, avoiding the double taxation faced by corporations.

1. For single-member LLCs, you will report business income on Schedule C of your Form 1040.

2. Multi-member LLCs file Form 1065 (US Return of Partnership Income) with the IRS. Each member will receive a Schedule K-1 detailing their share of profits or losses.

Let's consider this scenario. Your new limited liability company has a great year, earning $100,000 in profit. You decide to keep $60,000 in the business and distribute $40,000 to yourself. Come tax time, you are surprised to find that you owe taxes on the full $100,000, not just the $40,000 you took as a distribution. This is pass-through taxation in action where you are taxed on your share of profits, regardless of distributions.

For single-member limited liability companies, the IRS views your business as a disregarded entity for federal tax purposes.

1. All profits are reported on your personal tax return, whether distributed or not. You will typically use Schedule C (Profit or Loss from Business) to detail your business's income and expenses. This simplifies bookkeeping but can lead to higher personal tax liability.

2. You will likely owe self-employment tax (15.3%) on your LLC's net earnings. This covers Social Security and Medicare contributions, which are typically split between employers and employees.

3. It is crucial that you pay estimated taxes throughout the year as no taxes are automatically withheld from your LLC distributions. You need to estimate your income and pay both income tax and self-employment tax quarterly to avoid potential penalties at the end of the year.

4. You must consider exploring tax-advantaged retirement savings plans like a SEP IRA or Solo 401(k). Contributions to these plans are often tax-deductible, potentially reducing your current taxable income and offering long-term savings benefits.

In multi-member LLCs, the tax treatment of distributions can be more complex due to varying ownership structures.

1. Profits and losses are allocated among the members based on the terms outlined in your operating agreement. This allocation might not always be directly proportional to the actual cash distributed to each member.

2. Each member receives a Schedule K-1 from the LLC, which reports their share of the LLC's income, deductions, credits, etc. You must use the information on your K-1 to report your share of the LLC's financial activity on your personal tax return.

3. Understanding your ‘basis' in the LLC is important. It generally includes your capital contributions, share of the LLC's profits, and certain liabilities. Distributions are typically tax-free to the extent of your basis.

4. If the amount of cash distributed to you exceeds your basis in the LLC, the excess is usually taxed as a capital gain. For instance, if your basis is $5,000 and you receive a distribution of $7,000, the $2,000 exceeding your basis might be subject to capital gains tax.

While the default tax classification for an LLC is as a disregarded entity (for single-member) or a partnership (for multi-member), you have the option to elect to be taxed as either an S corporation (S-Corp) or a C corporation (C-Corp).

Here is how both scenarios work:

1. S-Corp election: With the S-Corp election, you can pay yourself a reasonable salary, just like any other employee. This salary is subject to payroll taxes (which include your self-employment taxes). The good news is that any remaining profits can then be distributed to you as the owner, and these distributions are not subject to self-employment tax. For example, if your LLC makes $100,000 in profit, and you pay yourself a $60,000 salary, you will only pay self-employment tax on that $60,000. This can potentially save you money on self-employment taxes.

2. C-Corp election: If you elect to be taxed as a C-Corp, your LLC is treated as a completely separate tax-paying entity. First, the C-Corp pays its own corporate income taxes on its profits. Then, if the C-Corp decides to distribute any of those profits to you (the shareholder) as dividends, you will have to pay taxes on those dividends as well. This is known as 'double taxation' where the profits are taxed once at the corporate level and again at the individual level. For most startups, this double taxation can be a significant disadvantage

You must also stay informed about updates that could affect your LLC's tax treatment. For instance, many states now offer pass-through entity (PTE) taxes as a workaround to the federal SALT deduction cap. These allow LLCs to pay state income taxes at the entity level, potentially providing significant tax savings.

Effectively managing LLC distributions is vital for your startup's financial health and legal compliance. Here are common pitfalls to avoid:​

1. Commingling personal and business finances: Mixing personal funds with LLC assets can compromise liability protection and complicate financial records. Maintain separate bank accounts and financial records for your LLC to preserve its legal integrity.

2. Neglecting the operating agreement: An outdated or vague operating agreement can lead to disputes among members regarding profit distribution. Regularly review and update this document to reflect current agreements and operational changes. ​

3. Failing to document distributions properly: Informal or undocumented distributions can raise red flags during audits and create misunderstandings among members. Always document distributions with clear records, including amounts, dates, and recipient details. ​

4. Insufficient tax provisioning: A critical mistake is distributing all available profits without setting aside an adequate amount to cover your tax obligations. Remember, you are taxed on your share of the profits, regardless of how much you distribute. Underestimating your tax liability can result in penalties.

From pass-through taxation to avoiding common pitfalls, managing your LLC's finances requires careful attention to detail and compliance with various regulations. Proper handling of distributions is essential for both legal compliance and maintaining positive relationships with your team members and investors.

At Qapita, we recognize the challenges startup founders face in managing equity and financial matters. Our comprehensive equity management platform, rated as #1 by G2, is designed to streamline these complex processes, allowing you to focus on growing your business. We offer robust tools for CapTable management, equity awards, and ESOP administration that can significantly simplify your LLC's financial operations.

We also provide expert advisory and consulting services to help you design and implement ESOP schemes that align with your company's goals and industry best practices. With Qapita, you can easily track distributions, maintain accurate records, and gain valuable insights for tax planning. Our platform also offers powerful scenario analysis tools for modeling future funding rounds or exits, ensuring you are always prepared for your next big move.

Ready to take control of your LLC's equity management? Discover how Qapita can help your startup thrive and manage its finances effectively. Book a 1:1 demo today.