Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

Ever wondered how the proceeds from a startup's exit are actually divided? It's rarely as simple as just splitting things by ownership percentages.

When a startup reaches a liquidity event like an acquisition, IPO, or secondary transaction founders often discover that investor terms and equity structures shape the final payout far more than expected. This is where waterfall analysis becomes essential.

In this guide, we'll break down how waterfall analysis works, walk you through an example step-by-step, and explain how tools like Qapita's scenario modeling simplify the process.

Waterfall analysis is a method for modeling how the proceeds from an exit flow down through a company's capitalization structure. Think of it like a sequence: certain investors get paid first, based on the terms of their investment, and the remaining value "flows" downstream to other shareholders.

For instance, a 1x liquidation preference means the investor gets their money back first. A 2x participating preference means an investor not only gets double their investment but also participates in the remaining proceeds with other shareholders. These mechanics deeply impact the payout that common shareholders including founders and employees ultimately receive.

Understanding these structures empowers founders to forecast outcomes, negotiate fairer terms during fundraising, and avoid disappointment when exits occur.

Getting familiarized with the key components of a waterfall model is essential for accurately determining how proceeds are distributed among various stakeholders during a liquidity event:

In a company's capital structure, stakeholders are typically categorized into:

1. Common Shareholders: These include founders, employees, and early investors who hold common stock. They usually have voting rights but are last in line to receive proceeds during a liquidation event.

2. Preferred Shareholders: Often institutional investors or venture capitalists, preferred shareholders have priority over common shareholders when it comes to distributions. They may also have additional rights and preferences outlined in investment agreements.

Liquidation preferences determine the order and amount of proceeds allocated to shareholders during a liquidity event, such as an acquisition or bankruptcy. They ensure that preferred shareholders recoup their investments before any distributions are made to common shareholders. For instance, a 1x liquidation preference means that the preferred shareholder is entitled to receive an amount equal to their initial investment before others participate in the remaining proceeds.

Dividends are payments made to shareholders from a company's earnings. In the context of a waterfall model, preferred shareholders might have the right to receive cumulative or non-cumulative dividends before any distributions are made to common shareholders. Cumulative dividends accumulate over time if unpaid, whereas non-cumulative dividends do not carry over if not declared.

Participation rights allow preferred shareholders to receive their liquidation preference and then share in the remaining proceeds alongside common shareholders. This is often referred to as "double-dipping." There are two main types:

1. Participating Preferred: After receiving their initial liquidation preference, these shareholders participate pro-rata with common shareholders in the remaining proceeds.

2. Non-Participating Preferred: These shareholders must choose between taking their liquidation preference or converting to common stock to share in the proceeds, but not both.

Conversion rights grant preferred shareholders the option to convert their preferred shares into common shares, typically at a predetermined ratio. This is advantageous when the value of common shares exceeds the value provided by the liquidation preference. Conversion rights are particularly significant during events like initial public offerings (IPOs), where converting to common stock might yield a higher return.

Before diving into a waterfall model, it's essential to understand the building blocks:

A company's cap table is the foundation. It outlines who owns what investors, founders, and employees via stock options/ RSUs etc. You'll also need to consider the specific terms attached to each shareholder class, especially around liquidation preferences and participation rights.

Convertible instruments such as SAFEs or convertible notes must be factored in. They typically convert into equity upon a trigger event like an exit, altering the ownership and payout distribution.

Lastly, you'll model various exit outcomes say, $20 million vs $100 million to understand how the waterfall shifts in each case.

To explore cap tables in more depth, visit: What is a Cap Table and Why Do You Need One?

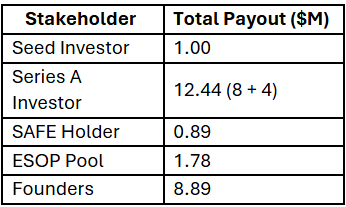

Let's Build One: Here's a practical example to illustrate how waterfall analysis works- Modeling an Exit from Start to Finish:

Company X has:

Step 1: Apply Liquidation Preferences The Seed investor receives $1M. The Series A investor, with 2x participating preferred, receives $8M. That's $9M accounted for.

Step 2: Distribute Remaining Proceeds There's $16M left after liquidation preferences. The remaining equity holders (excluding the Seed Investor) split it based on their relative ownership:

Final Payout Summary:

This example illustrates how preference terms and ownership structures can dramatically affect who walks away with what.

Accurate waterfall modeling is essential for determining the equitable distribution of proceeds among stakeholders during a company's liquidity event. However, several common mistakes can compromise the integrity of these models.

Incorrectly implementing liquidation preferences can lead to inaccurate payout calculations, disadvantaging certain shareholders. For example, applying specific terms intended for one limited partner (LP) to another can result in misallocations.

Failing to account for convertible securities like SAFEs and convertible notes can result in unexpected dilution and misallocation of proceeds. These instruments often convert to equity under specific conditions, impacting the overall distribution structure.

Omitting accrued dividends from preferred shares can distort the distribution hierarchy and lead to disputes. Preferred shareholders may be entitled to cumulative dividends that must be paid before any distributions to common shareholders.

Confusing participating and non-participating preferred stock can result in errors, such as double-dipping or unfair distributions. Understanding the specific rights associated with each class of stock is crucial to ensure accurate modeling.

Errors in modeling the conversion of preferred shares to common stock can lead to incorrect equity distribution. Misjudging the conversion ratios or thresholds can significantly impact the outcomes for various stakeholders.

Relying on static models that don't account for various exit scenarios can lead to unrealistic expectations and flawed decision-making. Dynamic modeling allows for simulation of multiple outcomes, providing a more comprehensive understanding of potential distributions.

Building waterfall models manually using spreadsheets increases the risk of errors, especially as the capitalization structure becomes more complex. Manual calculations are prone to mistakes such as incorrect formulas, data entry errors, and version control issues.

Many founders assume ownership percentage alone determines their final payout. That's a dangerous misconception.

Convertible instruments like SAFEs and notes, if not properly modeled, can lead to unexpected dilution. Founders may also underestimate how participating preferred shares reduce their take-home value. A 10% ESOP, for instance, can eat into founder equity post-liquidation.

To avoid such pitfalls, it's crucial to model realistic outcomes and update your cap table regularly. For deeper guidance, read: Best Practices for Cap Table Management

Building a waterfall model isn't just a financial exercise. It's a strategic tool. By forecasting different exit scenarios, founders can:

1. Clarifies Financial Outcomes: Waterfall analysis provides a clear, detailed breakdown of how exit proceeds will be allocated among various stakeholders, ensuring transparency and reducing potential disputes.

2. Informs Negotiations: Understanding potential financial outcomes allows companies to negotiate more effectively with investors and buyers, structuring deals that align with stakeholders' expectations.

3. Assesses Impact of Financial Instruments: The model evaluates how instruments like convertible notes and SAFEs will convert during an exit, highlighting their effect on equity distribution.

4. Aids in Strategic Decision-Making: Simulating various exit scenarios allows companies to make informed strategic decisions regarding the timing of the exit and valuation targets, ultimately optimizing stakeholder returns.

5. Enhances Stakeholder Communication: Providing stakeholders with detailed projections fosters trust and ensures that all parties have realistic expectations regarding their returns.

6. Understand how much they and their teams actually stand to earn: This clarity is invaluable during acquisition offers, investor negotiations, and team equity conversations. It also helps avoid conflict and surprises at the time of exit.

Scenario modeling ensures you raise capital and negotiate terms with foresight. Instead of reacting later, you're planning ahead today.

Instead of struggling with spreadsheets, Qapita offers a purpose-built solution:

Qapita's scenario modeling tools enable you to import your cap table, input investor terms such as liquidation preferences and convertible notes and visualize how proceeds will flow across various exit values. This empowers you to make informed decisions with confidence, ensuring optimal outcomes for all stakeholders.

Outputs are easy to share with your board or legal team. Book a free demo now!

For more information, explore: Qapita Scenario Modeling

Effectively communicating waterfall payouts is essential for ensuring that all stakeholders understand how proceeds will be distributed during a liquidity event. To achieve this clarity:

1. Develop a Clear Communication Plan: Outline what information needs to be shared, who is responsible for communicating it, and the timeline for dissemination. A structured plan ensures consistent and timely updates to all stakeholders.

2. Utilize Professional Cap Table Software: Employing specialized tools can help organize and present ownership details clearly, showing top shareholders and their respective ownership percentages. This approach enhances transparency and facilitates understanding among stakeholders.

3. Maintain Transparency: Clearly document and share the distribution process, ensuring that all transactions are conducted in line with agreed terms. Transparency fosters trust and reduces potential conflicts.

4. Establish a Feedback Loop: Provide stakeholders with opportunities to ask questions and offer feedback. This two-way communication helps identify and address concerns early, ensuring that all parties are aligned and informed.

Investors, board members, and acquirers want clarity. Your waterfall analysis should provide it. When presenting:

Use simple visuals to illustrate proceeds. Show multiple exit points for example, $10M, $25M, and $50M so stakeholders understand the full range of outcomes. Clearly explain your assumptions and how each stakeholder's rights affect the results.

Qapita's tools help founders present their payout structure professionally, instilling confidence with potential buyers and investors alike.

In VC-backed startups, waterfalls tend to be straightforward: preferred shares are paid out first, and common equity splits the rest. There may be participation rights, but the structure is relatively clean.

In contrast, private equity deals introduce new complexities. There may be minimum IRR hurdles (e.g., 8%) that must be met before anyone else is paid. Catch-up clauses and carried interest mechanisms further complicate the waterfall. PE sponsors might take 20% of profits above a threshold a significant shift in distribution logic.

Qapita is equipped to model both VC and PE scenarios, ensuring your equity story remains accurate as your business grows.

Waterfall analysis is more than just a spreadsheet it's a window into your company's financial outcome. The difference between assuming and knowing how much equity you'll walk away with can be millions of dollars.

As a founder, use waterfall modeling to inform how you raise capital, negotiate terms, and plan your company's exit. Don't wait until a term sheet lands to understand your outcome. Model it now.

Qapita makes this easier than ever, giving you clarity, confidence, and control.