Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Understanding regulatory requirements is essential if you manage a startup fund or plan to raise capital from investors. One key classification that affects fund managers is the Exempt Reporting Adviser (ERA) status. This designation allows certain investment advisers to operate under reduced regulatory obligations while still complying with investor protection laws.

The ERA classification was introduced as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. It aims to provide relief for smaller fund managers who do not manage extensive private fund assets. Unlike fully registered investment advisers, ERAs must file limited reports with the Securities and Exchange Commission (SEC) but are not subject to the same level of scrutiny and regulatory filings. This makes the designation attractive for emerging fund managers, including those managing private equity or venture capital funds.

If you are seeking capital from investment funds, it is important to understand how ERAs operate and what their status means for your fundraising efforts. This guide explores the key aspects of exempt reporting adviser status, including eligibility, compliance requirements, benefits, and limitations. Keep reading to learn more.

The ERA classification was introduced to balance regulatory oversight with the need for flexibility among smaller fund managers. Here are the key legislative and regulatory bodies that define the ERA landscape.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 reshaped financial regulations in the United States. This comprehensive legislation, enacted in response to the 2007-2008 financial crisis, introduced the concept of Exempt Reporting Advisers (ERAs). It was designed to reduce the compliance burden on smaller fund managers while maintaining investor protection.

Before this law was enacted, most investment advisers had to register with the SEC, regardless of the size of assets under management. The Dodd-Frank Act changed this by creating exemptions for advisers managing venture capital funds or private funds with less than $150 million in assets. This change allowed smaller fund managers, including those investing in startups, to operate with fewer regulatory constraints while still being subject to limited reporting obligations.

Understanding the origins of the ERA framework is essential for startup founders when evaluating potential investors. While ERAs must follow ethical and fiduciary standards, they do not face the same level of regulatory scrutiny as fully registered investment advisers. This makes it important for you to conduct due diligence when selecting investors or VC fund managers.

The SEC regulates investment advisers in the US. While ERAs are not required to register as fully regulated investment advisers, they must still comply with certain SEC rules. As an ERA, a fund manager must file reports detailing key operational information through the Investment Adviser Registration Depository (IARD) system.

As an ERA, a fund manager must file reports detailing key operational information through the Investment Adviser Registration Depository (IARD) system. While these filings are less extensive than those required for fully registered investment advisers, they still provide transparency regarding fund structure and management.

The SEC primarily monitors ERAs through periodic reviews and enforcement actions. If an exempt reporting adviser fails to comply with its obligations, the SEC can take action, which may include penalties or revocation of ERA status.

The recent SEC enforcement actions have increased the scrutiny of private fund advisers, emphasizing investor protection and compliance with anti-fraud regulations under the Investment Advisers Act of 1940.

Here are the two primary exemptions under which a venture capital adviser can qualify as an ERA.

The Private Fund Adviser Exemption is designed for investment advisers who solely manage private funds and have Assets Under Management (AUM) below a certain threshold. Here are the key points to understand:

a) AUM threshold: To qualify for this exemption, an adviser must have less than $150 million in assets under management in the United States.

b) Definition of private funds: Private funds are defined as funds that would be investment companies under the Investment Company Act of 1940, but for the exclusions provided by Section 3(c)(1) or 3(c)(7) of that Act. These typically include:

c) Calculation of AUM: The $150 million threshold is based on Regulatory Assets Under Management (RAUM), which includes:

d) Annual assessment: Advisers must annually assess their RAUM to ensure continued eligibility for the exemption.

The Venture Capital Fund Adviser Exemption is tailored for advisers who exclusively manage venture capital funds. This exemption does not have an AUM limit, but it does have specific requirements for what constitutes a venture capital fund:

a) Venture capital fund definition: The SEC defines a venture capital fund as a private fund that:

1. Represents itself to investors as pursuing a venture capital strategy

2. Holds no more than 20% of its aggregate capital contributions and uncalled committed capital in non-qualifying investments

3. Does not borrow or otherwise incur leverage more than 15% of the fund's aggregate capital contributions and uncalled committed capital

4. Only provides equity securities to its investors

5. Is not registered under the Investment Company Act and has not elected to be treated as a business development company

b) Qualifying Investments: These typically include equity securities of qualifying portfolio companies, which are generally private companies that are not themselves investment companies.

c) Non-qualifying investments: The 20% basket for non-qualifying investments allows for some flexibility in investment strategy, potentially including investments in public companies or other types of securities.

d) No AUM limit: Unlike the Private Fund Adviser Exemption, this exemption does not limit the amount of assets that can be managed.

Many venture capital firms structure their operations to remain within the limits of the Venture Capital Fund Adviser Exemption. For example, a VC firm that raises a $50 million fund to invest in early-stage technology startups could qualify under this exemption. Since it does not trade in public markets or use high leverage, it meets the SEC's definition of a venture capital fund.

Here are the key compliance requirements that ERAs must follow:

One of the primary compliance requirements for ERAs is the filing of Form ADV. This form serves as the official registration with the SEC and provides essential information about the advisory business. Here's what you need to know:

1. Initial filing: The adviser must file Form ADV within 60 days of relying on the ERA exemption. This initial filing establishes the ERA status with the SEC.

2. Annual updates: It is vital to update the Form ADV annually, within 90 days of fiscal year-end. For most ERAs with a fiscal year-end on December 31, this means filing by March 31 each year.

3. What to file: ERAs are only required to complete certain portions of Form ADV Part 1A. These include:

4. Public disclosure: The information provided in Form ADV is publicly available. ERAs must be accurate and thorough but also mindful of sensitive information.

5. Filing Method: All Form ADV filings must be submitted electronically through the Investment Adviser Registration Depository (IARD) system.

6. Filing Fees: While the SEC doesn't charge ERAs filing fees, they need to pay a fee to the Financial Industry Regulatory Authority (FINRA) for using the IARD system. As of 2025, this fee is $150 annually for ERAs.

The compliance obligations don't end with the annual Form ADV filing. ERAs have ongoing responsibilities to keep regulators informed:

1. Material changes: If significant changes to the business affect the accuracy of Form ADV, the ERA must promptly amend the form. This includes changes such as:

2. Monitoring assets under management: Regularly assess the RAUM, and if it exceeds the relevant thresholds ($150 million for private fund advisers or $25 million for venture capital fund advisers), ERAs may need to transition to full SEC registration.

3. Cybersecurity: As of 2025, the SEC has increased its focus on cybersecurity for all investment advisers, including ERAs. They must implement robust cybersecurity measures to protect client data and the firm's information.

4. Anti-Money Laundering (AML) program: As of January 2, 2026, both registered investment advisers and ERAs must comply with new AML and Countering the Financing of Terrorism (CFT) requirements. This includes implementing an AML program and filing Suspicious Activity Reports (SARs) when necessary.

5. State requirements: Some states may have additional reporting or compliance requirements beyond the SEC for state-level ERAs.

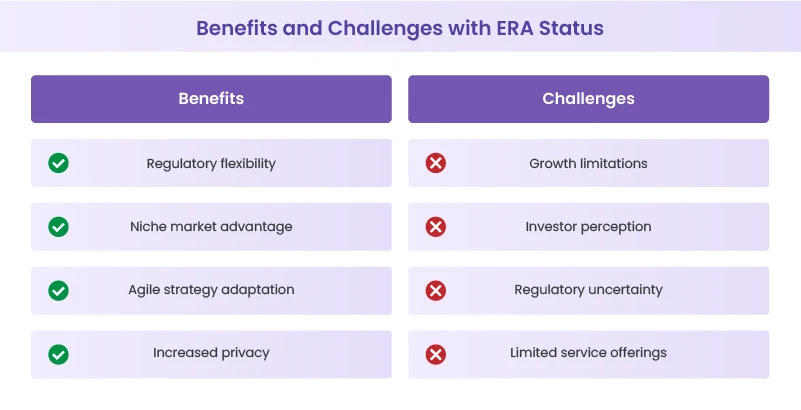

The ERA status presents both opportunities and challenges for fund managers and startup founders.

1. Regulatory flexibility: ERA status provides a middle ground between full SEC registration and complete exemption. This flexibility allows fund managers to operate with reduced regulatory oversight while still maintaining a level of credibility with investors who value some regulatory involvement.

2, Niche market advantage: ERAs often specialize in specific investment strategies or market segments. This focus can be a significant advantage when targeting investors seeking exposure to unique or emerging market opportunities that may be less accessible through larger and more diversified funds.

3. Agile strategy adaptation: With fewer regulatory constraints, ERAs can quickly adjust their investment strategies or fund structures in response to market changes. This agility can be particularly valuable in fast-moving sectors or during periods of market volatility.

4. Increased privacy: Compared to fully registered investment advisers, ERAs disclose fewer details about their clients, investment strategies, and fund performance. This provides an added layer of privacy, allowing them to operate with greater discretion

1. Growth limitations: The asset thresholds associated with ERA status (typically $150 million for private fund advisers) can create a growth ceiling. Managers must carefully consider the trade-offs between maintaining ERA status and pursuing expanded assets under management.

2. Investor perception: Some institutional investors have internal policies that favor or require investments with fully registered advisers. This perception challenge can limit an ERA's access to certain pools of capital, potentially affecting growth and diversification strategies.

3. Regulatory uncertainty: As a relatively new classification in regulatory terms, the ERA status is subject to potential changes in the regulatory landscape. Fund managers must stay vigilant and be prepared to adapt to evolving regulatory requirements, which can create operational uncertainties.

4. Limited service offerings: ERAs are restricted in the types of clients they can serve and the services they can offer. This limitation can constrain business expansion opportunities, particularly for firms looking to diversify their client base or service offerings.

Understanding when and how to transition from ERA to a Registered Investment Adviser (RIA) can help prepare for the next stage of the fund's growth.

Several factors can trigger the need for an ERA to transition to full registration as an investment adviser:

1. Exceeding the AUM threshold: One of the primary reasons fund managers transition from exempt reporting adviser status to full RIA registration is surpassing $150 million in AUM. If an ERA's AUM reaches this threshold, they must register with the SEC within 90 days after filing their annual updating amendment.

2. Expanding beyond private fund management: ERA status is granted to advisers who manage only private funds. If a firm starts offering advisory services to individual clients, institutional investors, or public market participants, it may be required to register as an RIA. Providing investment advice beyond the scope of private funds can trigger regulatory scrutiny, making full registration necessary.

3. Changes in the regulatory environment: Regulatory policies evolve, and the SEC periodically revises its rules governing investment advisers. If new policies tighten reporting or compliance requirements for ERAs, fund managers may need to reassess whether maintaining exempt status is still feasible. .

Some ERAs choose to register even before hitting these triggers, often to enhance credibility with investors or to prepare for future growth.

Moving from exempt reporting adviser status to a registered investment adviser involves significant operational adjustments. Understanding the process can help ensure a smooth transition while maintaining compliance.

1. Preparing for SEC registration: The first step in transitioning is submitting Form ADV to the SEC with expanded disclosures, including details about the firm's ownership, investment strategies, client base, and compliance practices. Unlike the limited version required for ERAs, this filing requires comprehensive reporting on all aspects of the firm's operations.

2. Implementing compliance policies: RIAs must establish and enforce strict compliance programs that align with SEC regulations. This includes creating written policies for recordkeeping, client communications, cybersecurity measures, and internal audits. Many fund managers hire compliance officers or work with legal advisors to ensure adherence to new regulatory requirements.

3. Adapting to new reporting obligations: RIAs must follow ongoing reporting and disclosure requirements, including annual Form ADV updates, periodic SEC examinations, and enhanced investor reporting. Implementing systems to track and manage compliance can help streamline these processes.

4. Managing operational changes: Transitioning to RIA status may require restructuring business operations, including adjusting internal workflows, adopting new technology solutions, and revising investment agreements. As compliance costs increase, fund managers may need to allocate additional resources to legal, administrative, and regulatory functions.

Understanding the role of an Exempt Reporting Adviser (ERA) is crucial for startup founders. ERAs operate under specific regulatory frameworks that offer reduced compliance obligations, making them an attractive option for emerging fund managers. However, as funds grow and evolve, transitioning to a Registered Investment Adviser (RIA) may become necessary to accommodate expanded operations and client bases.

At Qapita, we understand the complexities faced by startups and fund managers in managing their equity and compliance obligations. We specialize in simplifying equity management for startups and investment firms. Our equity management platform, rated as #1 by G2, offers comprehensive solutions for cap table management, ESOP administration, and valuation services, ensuring compliance with regulatory standards. By leveraging our tools, you can efficiently manage your equity structures and stay ahead of compliance requirements.

Book a 1:1 personalized demo with our experts to learn more about our solutions.