Equity management

Equity management

ESOP Management

ESOP Management- Fund management

Liquidity Solutions

Liquidity Solutions - Fund managementESOP Consulting

- Fund managementFund Management

Crafting an effective employee compensation strategy involves more than just salaries and bonuses. Equity compensation enables companies to draw in top talent, keep star performers, and tie employee motivations to sustain business success.

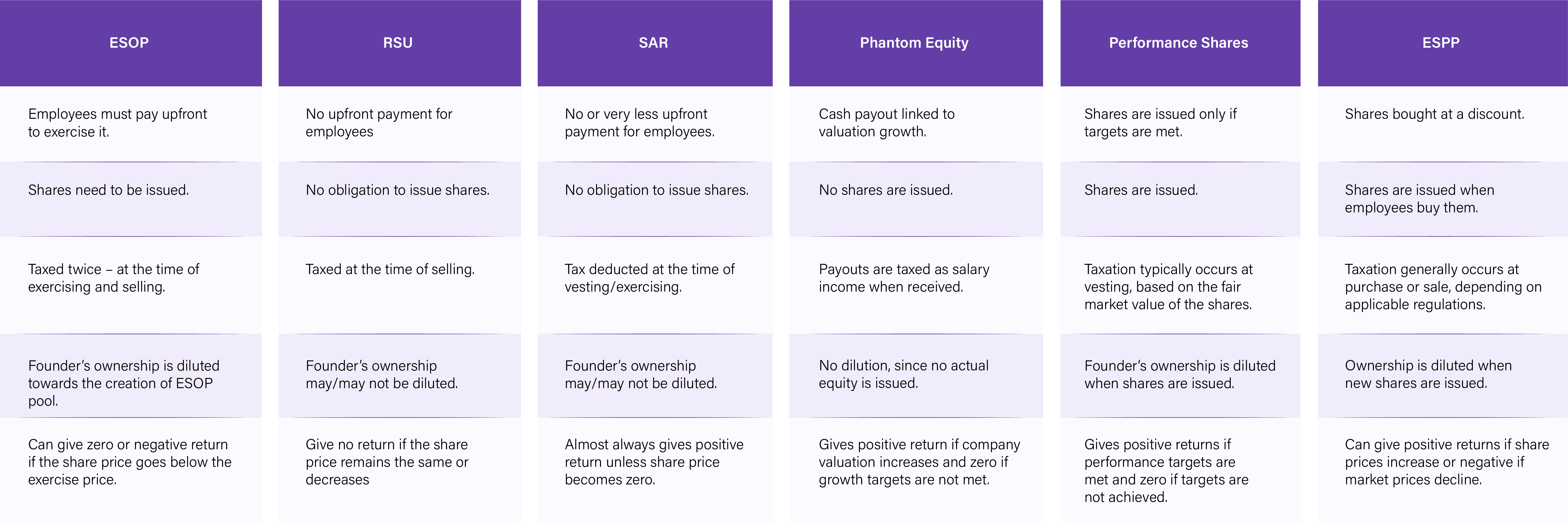

Startups and founders have several equity-based options, including Employee Stock Option Plans (ESOPs), Restricted Stock Units (RSUs), Stock Appreciation Rights (SARs), Phantom Equity, Performance Shares, and Employee Share Purchase Plans (ESPPs). These vary in mechanics and fit different company stages and financial situations.

Designing the right employee compensation strategy goes beyond salaries and bonuses. Equity-based compensation helps companies attract talent, retain high performers, and align employee incentives with long-term business growth.

In this guide, we break down different types of equity by explaining how they work, their pros and cons, and how to choose the right option for your company.

Employee stock options plan (ESOP) refers to an employee benefit plan under which a company grants stock options to its employees. Companies use ESOPs to attract and retain talent by allowing their employees to purchase shares of the company at a price fixed on the grant date.

The company grants a certain number of stock options to employees (stock grantees), which vest over a certain period. Once stock options get vested, employees can purchase shares by paying the exercise (strike) price. The exercise price is usually lower than the market price (fair market value), which results in a notional income for the employees and taxed as income from salary.

The notional income is calculated as the difference between shares fair market value (FMV) and the exercise price.

Notional income = Market value of shares - Amount paid by the employee

The employees need to pay the tax on this notional income based on their tax bracket. Furthermore, when employees sell the shares, they are taxed again. This is considered as a capital gain for the period during which they hold the shares. The difference between sales value and the fair market value of the shares at the time of exercise is considered a capital gain.

Income from capital gain = Market value at the time of selling the shares - Market value of the share at the time of exercising the shares

Stage 1: At the time of exercise

Notional/Perquisite income from options = Difference between the fair market value of stock and exercise price * Number of the options exercised Tax on perquisite income = Tax as per regular slab rate for individuals

Stage 2: At the time of sale of the shares

Capital gain on sale of shares

• Short-term capital gains when shares are held less than 12 months.

• Long-term capital gains when shares are held more than 12 months

• Short-term capital gains when shares are held less than 24 months.

• Long-term capital gains when shares are held more than 24 months

ESOPs come with complex rules and regulations and require companies to maintain accurate records. Qapita, an equity management tool, makes it easy to grant and administer ESOPs.

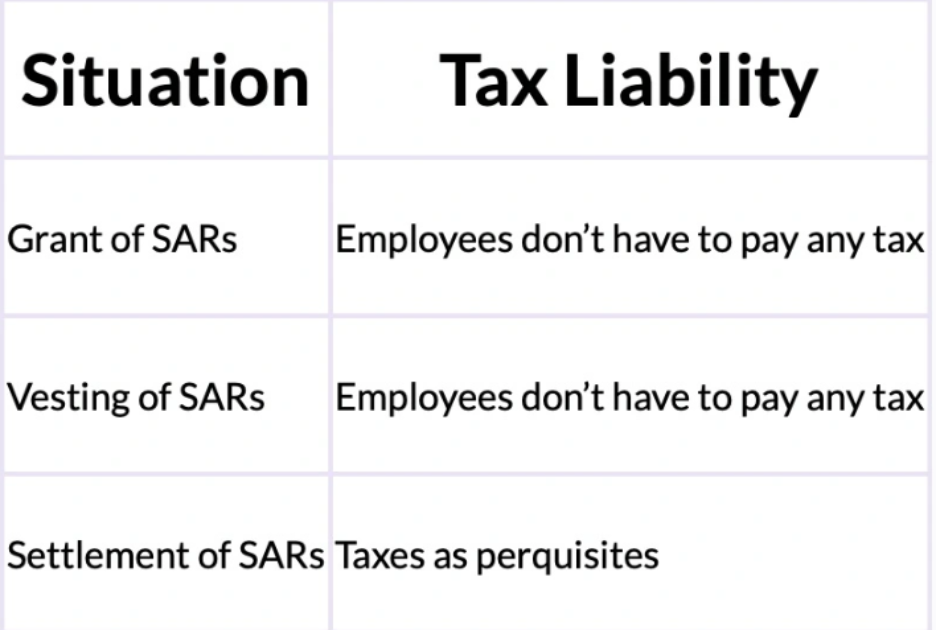

Stock appreciation rights (SARs) is another employee compensation method in which employees are given an amount equal to the appreciation in the value of the shares over a specific period.

This amount is equal to the difference between the market price on the date of vesting and the strike price and is settled in cash or shares.

For example, consider an employee who earns 1000 SARs. The SARs vest after 3 years and the price of the share increases from Rs 500 to Rs 700 during this time. Then, the employee receives an amount equal to Rs 200,000 (1000*(700-500)).

Employees do not have to pay any amount (the exercise price), and it automatically gets vested after completion of the period. The perquisite received is taxed as the salary income on the employee's tax slab.

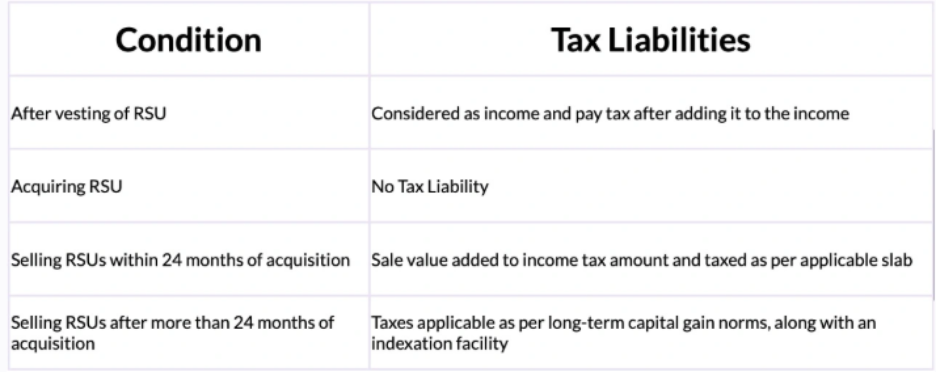

Restricted stock units (RSUs) are another type of compensation benefit for employees. They are deeply discounted options usually given at the face value and often granted to the employees based on their performance.

They have a predefined vesting period or targets and get automatically vested based on their completion.

Note there is a major difference in how RSUs work in India and the US. In India, though the strike price is very low compared with the market price, employees still have to exercise the option by paying the face value of the share.

On the other hand, in the USA, RSUs are stocks that employees own as they vest. Employees don't need to purchase them. Unlike in India, it's a one-step process in the US, as there is no concept of exercising in RSUs.

Phantom equity plans let employees cash in on a company’s growth and success without receiving actual shares. They come in two main forms: appreciation-only versions that pay out just the rise in stock value over time, and full-value plans that include the starting value plus all the gains. These plans link rewards directly to how well the company performs, giving the feel of true ownership, without diluting founders' or existing shareholders' ownership. Since payouts are made in cash, they are taxed as ordinary income and are most commonly used as a long-term retention tool for senior leadership and key executives.

Phantom equity is taxed when the payout is actually made to the employee, not when the award is granted. Since employees receive cash instead of real shares, the payout is treated as salary or bonus income. This means it is taxed at the employee’s applicable income tax rate and may also be subject to payroll taxes. There are no capital gains benefits, because no actual shares are issued or sold.

Performance shares are a performance-based equity compensation tool granted to managers and senior employees when predefined business or financial targets are met.

Often issued as stock bonuses or equity-linked incentives, performance shares are designed to align employee objectives with shareholder value creation. The allocation and value of performance shares depend on the company’s performance and typically include a vesting period to promote long-term retention and sustained growth. There are two types of performance shares, namely, Performance Stock Units (PSUs) and Performance Stock Awards (PSAs).

A Performance Stock Unit (PSU) is an employer’s promise to grant shares once performance conditions are met and the vesting date is reached. A Performance Stock Award (PSA) is granted earlier, but like PSUs, the shares are delivered only after vesting and performance certification.

PSUs

When your shares vest, they are assigned a fair market value (FMV), and this value is treated as regular income or tax purposes. Your employer reports this amount on the applicable tax statement, and it is taxed just like your salary. In most cases, the company withholds the required taxes at the time of vesting, either by deducting cash or by retaining a portion of their shares, depending on how your equity plan is structured.

When you sell your shares, any change in value from the vesting date results in a capital gain or loss. A higher sale price results in a taxable gain which is equal to the difference between the sale value and the FMV at vesting, while a lower price leads to a capital loss.

If the shares are sold within one year, they are taxed as short-term capital gains at your regular income tax rate, while shares that are held for more than a year qualify for long-term capital gains, which are normally taxed at a lower rate. Since tax treatment can vary, consulting a tax professional is recommended.

An employee stock purchase plan (ESPP) allows employees to buy shares of their company at a discounted price, often up to 15%. Instead of purchasing the stock outright, employees contribute gradually through automatic deductions from their salary.

There are two types of ESPPs, namely qualified and non-qualified plans.

To implement an employer-sponsored qualified plan, shareholder approval is required. All eligible participants must receive equal rights, the discount offered is capped by regulation, and the offering period cannot exceed three years.

In contrast, non-qualified plans face fewer regulatory restrictions than qualified plans, offering greater flexibility. However, this flexibility comes at a cost, as non-qualified plans typically carry less favorable tax treatment.

The taxation of ESPPs can be complex. In most cases, taxes apply in the year the shares are sold, with the outcome treated either as taxable income or a deductible loss, depending on the transaction.

The gap between the purchase price and the sale price is treated as a capital gain or loss. Any discount received on the stock is taxed as ordinary income, while the remaining profit qualifies as a long-term capital gain. However, if the shares are sold before one year from the transfer date or within two years of the option grant, the entire gain is taxed as ordinary income.

Understanding your equity type is just the first step. Actually tracking it, knowing your vesting schedule, what you owe in taxes, and what your shares are worth today, is where things get complicated.

Qapita makes that part simple. ESOPs, SARs, RSUs, ESPPs - every company does equity differently. It brings it all into one place, giving you a clear, real-time view of your equity without the spreadsheets, the back-and-forth with HR, or the confusion at tax time.

Book a demo to see how Qapita can simplify equity management.