Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

Stock options are a critical component of startup compensation, offering employees the potential to benefit from a company's growth. One approach that is steadily gaining traction is the early exercise of stock options. This strategy allows employees to purchase their options before they fully vest, potentially reducing tax liabilities and increasing long-term gains.

As a startup founder, understanding how early exercise stock options function can help structure attractive equity plans that align with both employee and your company's interests. Many startup employees opt for early exercise to mitigate future financial risks and capitalize on lower valuation points. For founders, offering this option can serve as a strong incentive, enhancing employee retention.

This blog explores the mechanics of early exercise stock options, their key benefits, potential risks, tax implications, and best practices for structuring them effectively. Let's start!

Early exercise stock options are a unique form of equity compensation that allows employees to purchase their stock options before they vest. This means your team members can become shareholders in your company earlier than with traditional employee stock option plans, subject to approval of the company's board of directors.

When you offer early exercise stock options, you are giving your employees the right to buy shares of company stock at the strike price immediately after the options are granted rather than waiting for the vesting period to elapse.

The shares of the underlying stock purchased through early exercising are typically subject to a repurchase agreement. This agreement gives your company the right to buy back unvested shares at the original purchase price if the employee leaves before their vesting date. These shares of stock are often referred to as 'restricted shares' until they fully vest.

Early exercise fundamentally alters the traditional stock option model. Instead of waiting years for options to vest before exercising, employees can become shareholders from day one. This can create a stronger sense of ownership and alignment with your company's goals.

Various types of stock options can be eligible for early exercise:

1. Incentive Stock Options (ISOs): These tax-advantaged options are exclusively for employees. Early exercise of incentive stock options can lead to significant tax benefits, particularly if your company's value increases. By exercising early, employees may qualify for long-term capital gains treatment on the entire appreciation, potentially saving thousands of dollars in taxes.

2. Non-Qualified Stock Options (NSOs): These flexible options can be offered to employees, contractors, or advisors. The early exercise of non-qualified stock options helps manage tax liabilities by allowing holders to start the capital gains holding period sooner. This strategy can be particularly beneficial if you anticipate rapid growth in your company's valuation.

3. Restricted Stock Units (RSUs): While not technically 'exercised,' some companies offer early settlement of RSUs. This approach allows employees to receive shares sooner, potentially starting their holding period for capital gains purposes earlier. However, it is essential to note that restricted stock units are typically subject to immediate taxation upon vesting.

4. Restricted Stock Awards (RSAs): These are outright grants of stock subject to vesting. Early exercise concepts applied to RSAs allow employees to receive and own these awards sooner. This can be advantageous for tax purposes, as employees can file an 83(b) election to recognize income on the option grant date rather than as the shares vest.

By offering early exercise across these equity instruments, you provide your team with flexibility and potential financial benefits.

Here is an analysis of the risk-reward dynamics of these approaches and how they shift the balance of potential gains and losses for your company:

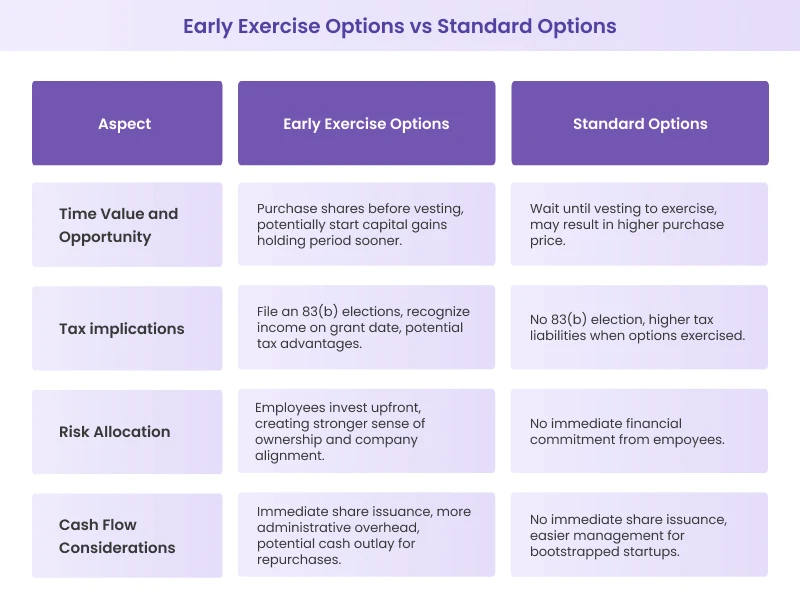

1. Time value and opportunity: Early exercise of an options contract allows employees to purchase shares before they vest, potentially starting the capital gains holding period sooner. Standard options, on the other hand, typically require employees to wait until vesting before exercising. If your company's value increases significantly over time, this may result in a higher stock price.

2. Tax implications: With early exercise, employees may be able to file an 83(b) election, recognizing income on the date of grant rather than as the shares vest. Standard options don't offer this benefit, potentially resulting in higher tax liabilities for employees when they eventually exercise their options.

3. Risk allocation: Early exercise shifts more risk to the employee. They are investing their own money upfront, betting on the company's future success. This can create a stronger sense of ownership and alignment with your company's goals. Standard options, while still providing motivation, don't require this immediate financial commitment from employees.

4. Cash flow considerations: Standard options may be preferable for bootstrapped startups as they don't require immediate share issuance or management of actual stockholders. Early exercisable options, while potentially more attractive to employees, require more immediate administrative overhead and a potential cash outlay for stock repurchases if employees leave before vesting.

Here are some unique aspects to consider while leveraging early exercise stock options to enhance your compensation strategy:

1. Competitive advantage in talent wars: In the current market, where top talent can be scarce, early exercise options can be a useful tool. They offer a unique value proposition that goes beyond just monetary compensation, appealing to candidates who are looking for long-term growth opportunities.

2. Cash flow management: Early exercisable stock options can help manage your startup's cash flow effectively. By offering equity compensation with early exercise, you can potentially reduce the need for high cash salaries, preserving your runway while still attracting top talent.

3. Company valuation impact: When employees exercise their options early, it can positively impact your company's valuation. This influx of cash can be seen as a vote of confidence by investors and can potentially lead to more favorable terms in future funding rounds.

4. Flexibility in exit scenarios: The early exercise feature can provide more flexibility in various exit scenarios. For instance, in an acquisition, having more employees as actual shareholders (rather than option holders) simplifies the process and leads to better outcomes for all parties involved.

5. Attracting experienced executives: Offering early exercise options can be particularly effective for key leadership positions. Experienced executives often understand the potential value of equity and may be more attracted to roles that offer them the opportunity to become significant shareholders early on.

Here are some unique scenarios and considerations to help you determine when early exercise makes the most sense:

1. Pre-funding rounds: Consider offering early exercise options before significant funding rounds. This allows employees to invest at a lower valuation, potentially increasing their long-term gains and aligning their interests with the company's growth trajectory.

2. Key milestones achievement: Tie early exercise opportunities to the achievement of critical company milestones. This approach rewards employees for their contributions to significant progress and reinforces the link between individual effort and company success.

3. Pre-IPO planning: As your company approaches a potential IPO, early exercise can be strategically valuable. It allows employees to start their capital gains holding period earlier, potentially leading to more favorable tax treatment when the company goes public.

4. International expansion: When expanding into new markets, early exercise options can be an effective way to attract and retain local talent. They demonstrate your commitment to long-term growth in the region and offer employees a stake in the company's global success.

5. Merger or acquisition prospects: If your startup is considering a merger or acquisition, early exercise options can simplify the process. Having more employees as shareholders rather than option holders can streamline negotiations and align interests.

6. Company pivot or restructuring: Offering early exercise options during significant strategic shifts can reinforce employee buy-in and demonstrate your commitment to shared success as the company navigates new directions.

As a startup founder, understanding the benefits and risks of early exercise stock options is crucial for making informed decisions about your company's equity compensation strategy.

1. Tax advantages: By exercising options early, your employees can start the capital gains holding period sooner. This means that if your company's value increases substantially, they may qualify for long-term capital gains treatment on a larger portion of their gains. For Incentive Stock Options (ISOs), early exercise can lead to more favorable tax treatment under the Alternative Minimum Tax (AMT).

2. Talent attraction and retention: Offering early exercise options demonstrates your commitment to employee ownership and can provide a unique value proposition that sets your startup apart. Employees who have invested their own money in the company are more likely to stay committed during challenging periods, providing stability to your workforce.

3. Accelerated innovation and risk-taking: Early exercise options can foster a culture of innovation and calculated risk-taking within your startup. When employees have a significant stake in the company from the outset, they are more likely to propose and champion bold ideas. This ownership mentality can lead to breakthrough innovations as team members feel empowered to think outside the box and take calculated risks.

4. Enhanced transparency and trust: By allowing employees to become shareholders early on, you are effectively opening up your company's financial and operational details to a broader internal audience. This increased transparency can lead to more informed decision-making at all levels of the organization. It also fosters a culture of trust, as employees feel they are genuinely part of the inner circle.

1. Financial risk for employees: Early exercise requires employees to invest their own money upfront, betting on the company's future success. This shifts more risk to the employee than traditional options. If your company's value decreases or fails to grow as expected, employees who exercise early may find themselves in a less favorable financial position.

2. Complexity and administrative burden: Implementing an early exercise program involves more administrative and legal complexity than standard options. You need to manage repurchase agreements, deal with the intricacies of 83(b) elections, and potentially handle more complicated tax reporting. This can increase your administrative overhead and may require additional resources to manage effectively.

3. Potential for underwater options: In volatile markets or industries, there is a risk that your company's value might decrease after employees have exercised their options. This can lead to a situation where the exercise price is higher than the current Fair Market Value (FMV) of the shares, commonly referred to as 'underwater' options. This scenario can be demoralizing for employees and may negate some of the intended benefits of your equity compensation strategy.

Here is an analysis of the tax aspects for Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs):

When your employees early exercise ISOs, they can potentially avoid AMT implications. Here is how:

1. If they exercise immediately after the grant and file an 83(b) election, the spread between the FMV and strike price is often $0, resulting in no AMT impact.

2. Without an 83(b) election, AMT is calculated on the spread between FMV and strike price at vesting, not at early exercise.

3. For qualifying dispositions (held two years from grant and one year from exercise), the entire gain is treated as long-term capital gain.

Early exercise of NSOs can offer significant tax advantages:

1. With an 83(b) election, employees pay ordinary income tax on the spread at exercise, which is often minimal or zero for early-stage startups.

2. This starts the clock for long-term capital gains treatment, potentially reducing future tax liability.

1. Timing matters: Exercising early in the calendar year gives more flexibility for tax planning.

2. AMT credit: If AMT is triggered, it generates a credit that can offset future regular tax liability.

3. Risk assessment: Early exercise involves financial risk if the company's value decreases or fails to grow as expected.

Early exercise stock options offer potential tax benefits, align employee interests with company goals, and can be a key differentiator in attracting and retaining top talent. However, implementing an early exercise program requires careful consideration of various factors, including tax implications, financial risks, and administrative complexities.

At Qapita, we specialize in helping startups like yours manage all aspects of equity compensation. Our equity management platform, rated #1 by G2, offers solutions for cap table management, equity awards, valuations, and advisory services tailored to your specific needs.

We understand the unique challenges startups face in managing equity. That is why we have partnered with leading organizations to ensure that you have the resources needed to succeed at every stage of your journey.

We invite you to reach out for a personalized consultation with our experts to discuss how Qapita can support your startup's growth and equity management needs.