Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Equity compensation, especially Restricted Stock Units (RSUs), has become a popular tool for startups to attract and retain top talent. However, traditional RSUs can present challenges, especially for private companies where immediate liquidity is not available.​

In many private companies, issuing standard RSUs means employees may face tax obligations upon vesting, even though they cannot sell shares to cover these taxes due to the absence of a public market. This situation can lead to financial strain for employees and complicate your compensation strategy.​ To address this issue, you can consider adopting double-trigger RSUs.

Unlike single-trigger RSUs that vest solely based on time or performance milestones, double-trigger RSUs require two specific conditions to be met before employees gain full ownership of the company shares. This approach ensures that employees are not burdened with tax liabilities before they can liquidate their shares. This blog examines the various aspects of double-trigger RSUs, including their operation, benefits, challenges, tax implications, and more.

Double-trigger RSUs stand out because they introduce an additional layer of criteria beyond just time for your employees to fully own their granted equity. Unlike any other form of equity compensation that might vest sooner, these RSUs require the fulfillment of two specific conditions before they are released.

The first condition in double trigger RSUs typically involves a time-based vesting schedule. This encourages employee retention and long-term commitment to your startup. A common approach is monthly vesting over four years, often with a one-year cliff. The cliff vesting schedule means that your employee must remain with the company for at least one year before any shares begin to vest.

For example, you might grant an employee 4,000 RSUs that vest monthly over four years, with a one-year cliff. After one year, 1,000 RSUs would vest, followed by approximately 83 RSUs each month thereafter. This type of equity compensation structure encourages employees to remain with your company for the long term, contributing to stability and continuity within your workforce.

The second condition usually relates to the occurrence of a liquidity event, such as an Initial Public Offering (IPO) or acquisition of your company. Private companies like yours often utilize this second trigger to strategically delay the point at which your employees face taxation on their vested equity.

By tying vesting to a specific event, you ensure that employees only receive liquid assets. This alignment of interests can be powerful, motivating your team to work towards a successful exit. However, it's essential to consider the potential risk that if a liquidity event does not occur, employees may never receive the full value of their RSUs, even after years of service.

When your employees' double-trigger RSUs vest, the shares are not immediately taxable. Taxation as ordinary income occurs only after the second trigger (liquidity event) is met. The taxable amount equals the Fair Market Value (FMV) of these shares at vesting. Preparing your team for potentially substantial tax obligations after an IPO or acquisition is crucial for effective financial planning.

With these restricted stock units, your employees do not incur immediate taxes upon completion of their time-based vesting schedule. Instead, taxation occurs only after a liquidity event, such as an IPO or acquisition. This structure provides a significant advantage, as your employees owe taxes at the moment when shares become liquid and can be sold to cover the resulting tax bill.

For instance, if your company goes public in year 4, all vested RSUs become taxable in that year rather than being taxed annually as they vest. This can be particularly advantageous for your employees in terms of tax planning and cash flow management.

In contrast, single-trigger RSUs trigger taxes as soon as they vest, often forcing employees to pay taxes on illiquid shares. The delayed tax liability of double-trigger RSUs aligns employee interests closely with your company's financial milestones, reducing the risk of financial stress for your team.

Despite clear benefits, double trigger RSUs can result in significant tax challenges for your employees. If your company's share price surges dramatically upon an IPO, employees might face unexpectedly large tax bills, given the high market value of their newly vested shares.

For instance, let's consider that your company grants an employee 10,000 RSUs that vest over a four-year period. If an IPO happens in year 4 when the value of the shares is $50, the employee will have $500,000 of taxable income in a single year. This sudden spike in income could push them into a higher tax bracket, resulting in a larger-than-expected tax bill.

Additionally, be mindful of the ‘must be present to win' clause. If an employee leaves before the liquidity event, they may forfeit their unvested RSUs, even if they have met the time-based vesting conditions. This could mean missing out on significant value if your company goes public or is acquired shortly after their departure.

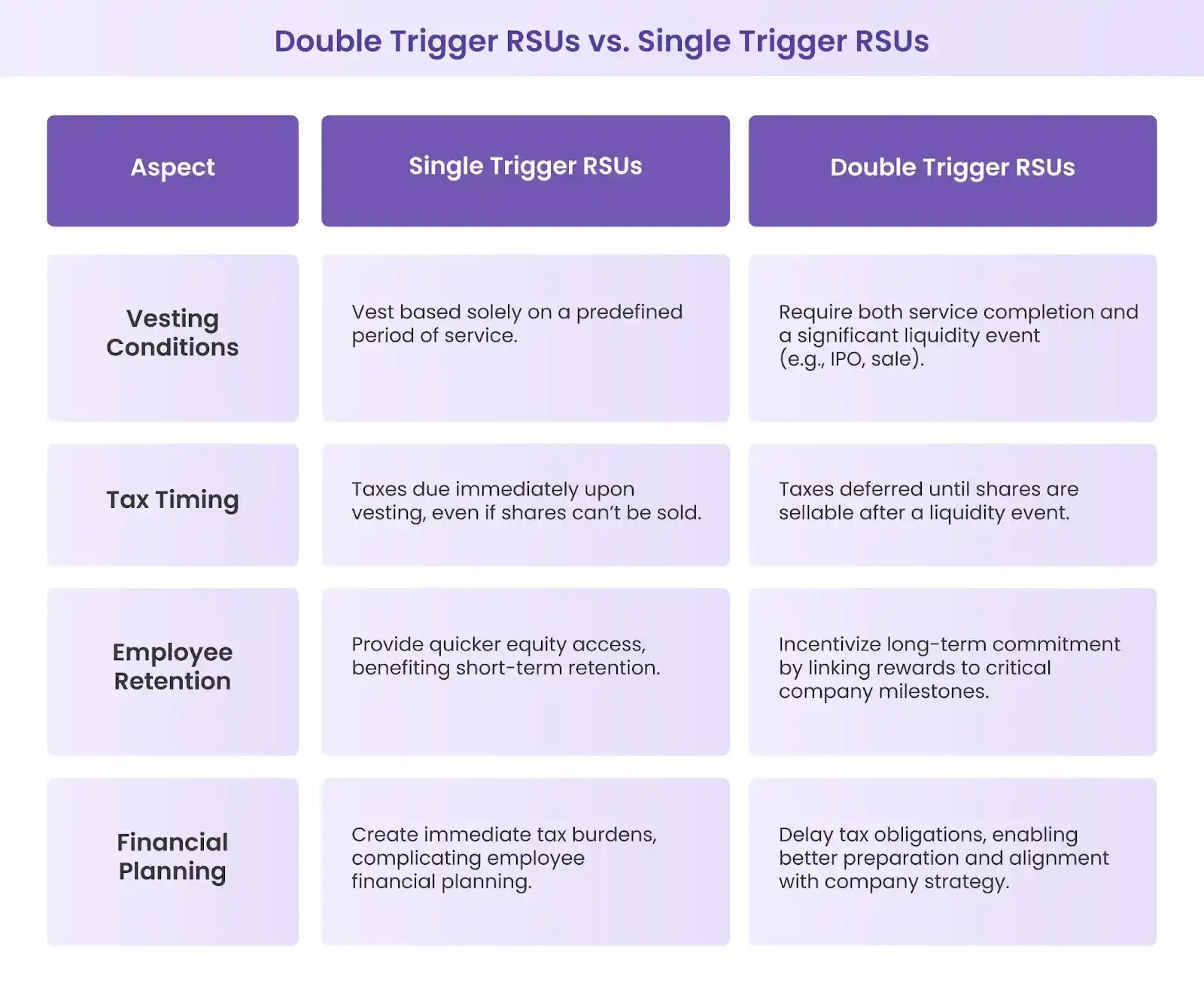

When choosing equity incentives for your startup, understanding how double-trigger RSUs differ from single-trigger RSUs helps you design a compensation strategy aligned with your company's goals and employees' needs.

1. Vesting conditions: Single trigger RSUs vest based solely on a predefined period of service. Double-trigger RSUs require both service completion and a significant event, such as an IPO or company sale.

2. Tax timing: Employees pay taxes immediately upon vesting with single-trigger RSUs, often facing taxes on shares they cannot yet sell. Double trigger RSUs defer taxes until the given number of shares are sellable after liquidity events.

3. Employee retention: Single trigger RSUs provide quicker equity access, benefiting short-term retention. Double-trigger RSUs incentivize long-term employee commitment by linking substantial rewards to key company milestones, such as acquisitions or IPOs.

4. Financial planning: Single trigger RSUs create immediate tax burdens, complicating financial planning for employees. Double-trigger RSUs delay these obligations, enabling better preparation and alignment with your startup's overall financial strategy.

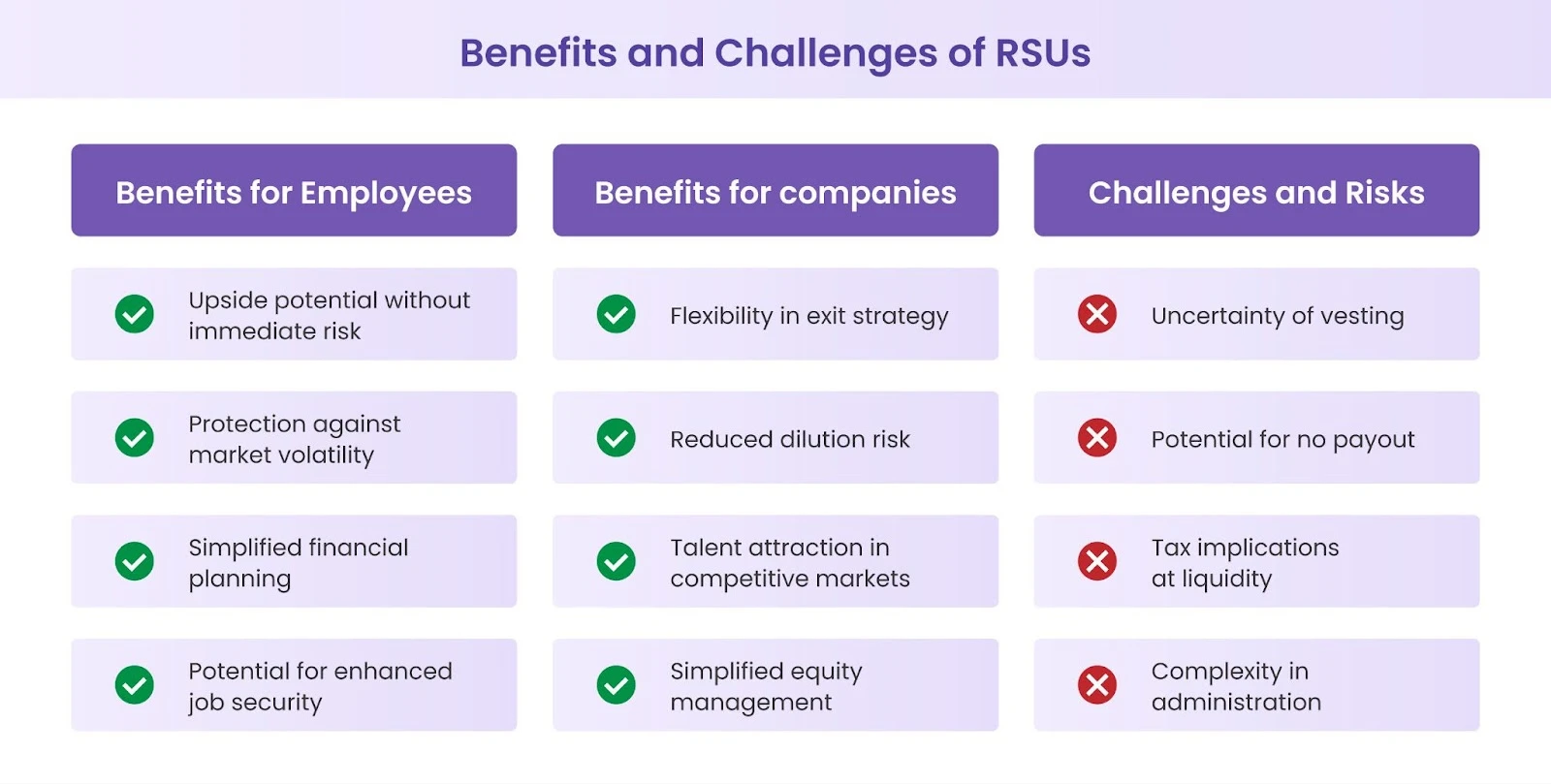

Double-trigger RSUs offer a unique set of advantages and potential drawbacks that are crucial for you to consider when structuring your compensation packages.

1. Upside potential without immediate risk: Employees can participate in your company's growth without the need for an upfront investment, unlike stock options, which may require purchasing actual shares. This allows them to benefit from potential stock appreciation without putting their finances at risk.

2. Protection against market volatility: The delay in share issuance until an exit event can shield employees from short-term market fluctuations, enabling them to focus on the company's long-term success. This structure encourages a more stable and committed workforce, less likely to be swayed by temporary market conditions.

3. Simplified financial planning: With taxation deferred until the liquidity event, employees can more easily plan for the financial impact of their equity compensation. This delay allows time to consult with financial advisors and develop effective strategies to manage the eventual tax implications.

4. Potential for enhanced job security: The dual-trigger structure may provide a level of protection against involuntary termination, as companies often accelerate vesting in the event of a change in control. This can offer employees a sense of security, knowing their equity is safeguarded even in times of organizational change.

1. Flexibility in exit strategy: Double-trigger RSUs allow you to maintain control over the timing and nature of liquidity events, providing strategic flexibility in planning your company's future. This structure enables you to align equity compensation with your long-term business goals and preferred exit scenarios.

2. Reduced dilution risk: By tying the second trigger to a liquidity event, you can avoid diluting your cap table with vested shares before a significant company milestone is achieved. This helps maintain a cleaner capitalization structure and potentially more attractive metrics for future investors or acquirers.

3. Talent attraction in competitive markets: Offering double-trigger RSUs can set your compensation package apart in highly competitive talent markets, especially for key executive positions. This unique structure can be a powerful tool for attracting top-tier talent who seek both immediate value and long-term growth potential.

4. Simplified equity management: Compared to other equity instruments like stock options, double-trigger RSUs can be simpler to administer and explain to employees, potentially reducing administrative overhead. This can lead to cost savings and fewer resources dedicated to managing your equity compensation program.

1. Uncertainty of vesting: The second trigger, a liquidity event, is not guaranteed. If your company does not go public or get acquired, employees might not realize the value of their double-trigger RSUs.

2. Potential for no payout: If an employee leaves before both triggers are met, they typically forfeit their unvested RSUs, even if they contributed significantly to the company's growth.

3. Tax implications at liquidity: Although tax is deferred, the tax burden at the time of the liquidity event can be substantial if the company's valuation has increased significantly.

4. Complexity in administration: Implementing and managing double-trigger RSUs can be slightly more complex than single-trigger RSUs, requiring careful documentation and tracking of both vesting schedules and trigger events.

Double-trigger Restricted Stock Units (RSUs) create a unique alignment between your employees' interests and your company's long-term success. Their structure encourages your team to think and act like owners, fostering a culture of innovation and dedication that can propel your startup toward its ultimate goals.

The dual-trigger mechanism offers a strategic advantage in talent retention, which is particularly crucial in competitive markets where rivals constantly court top performers. By requiring both time-based vesting and a liquidity event for full realization, you incentivize key employees to stay the course through critical growth phases, ensuring continuity in leadership and expertise. This can be especially valuable as you navigate the challenging path towards an IPO or acquisition, where stability in your core team can significantly impact investor confidence and deal outcomes.

Double-trigger RSUs also provide an elegant solution to the common problem of paper millionaires, employees rich in equity but cash-poor due to tax obligations on illiquid shares. By deferring both vesting and taxation until a liquidity event occurs, you protect your team from potential financial strain and allow them to focus on driving the company's success.

Understanding the intricacies of double-trigger RSUs is just the first step. Effectively managing and administering these equity grants is crucial for your startup's success. This requires careful tracking of both time-based vesting schedules and the occurrence of a qualifying liquidity event. This complexity can be a challenge for growing companies, potentially leading to administrative burdens and the risk of errors if not handled efficiently.

This is where Qapita comes in. We provide a comprehensive equity management platform, rated as #1 by G2, designed to simplify the complexities of managing equity, including sophisticated instruments like double-trigger RSUs. Our tools enable you to seamlessly track vesting schedules, manage your cap table with precision, and model various liquidity scenarios, providing a clear and real-time view of your company's equity. Our team is ready to provide expert guidance on structuring your Double Trigger RSU program, navigating complex scenarios, and optimizing your equity strategy from inception to IPO.

Contact us today for a personalized demo and discover how Qapita can streamline your equity compensation processes.