Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

Navigating the complexities of raising capital as a founder requires understanding legal frameworks like Regulation D of the Securities Act of 1933. This regulation includes Rule 506(b) and Rule 506(c), two essential pathways for startups to raise capital without the need to register securities with the Securities and Exchange Commission (SEC).

As a founder, choosing between Rule 506(b) vs 506(c) can significantly impact your capital raising strategy in the United States. Both rules offer exemption from securities regulations for private placements of securities. However, each rule comes with its own set of requirements and restrictions that can significantly affect your fundraising process.

This blog covers the key differences between Rule 506(b) vs 506(c) to help you make informed decisions about structuring your offerings and approaching potential investors. Let's get started.

Regulation D is a set of rules established by the SEC that provides exemptions from the registration requirements of the Securities Act of 1933. Its primary purpose is to facilitate capital formation for smaller companies by simplifying offerings of securities through private placements.

Within Regulation D, Rule 506 is vital for startups. It provides a safe harbor for private placement exemptions under Section 4(a)(2) of the Securities Act. This means that if you comply with the requirements of Rule 506, your offering will be deemed to comply with Section 4(a)(2).

Rule 506 is further divided into two subcategories, 506(b) and 506(c), which outline distinct pathways for conducting private securities offerings. General requirements that apply to both 506(b) and 506(c) offerings include:

Rule 506(b) under Reg D is a popular choice for private securities offerings, especially for startups that rely on relationship-based fundraising. One of its defining features is the prohibition on the use of general solicitation, meaning you cannot advertise or publicly promote your offering. This requires you to rely on a pre-existing substantive relationship with potential investors or work through trusted networks.

This rule allows you to accept investments from an unlimited number of accredited investors and up to 35 non-accredited investors. Accredited investors can self-certify their accreditation status, reducing your business's administrative burden.

For non-accredited investors, you must determine that they have sufficient knowledge and experience in financial and business matters to evaluate the risks and merits of the investment. This evaluation is crucial for compliance with SEC rules.

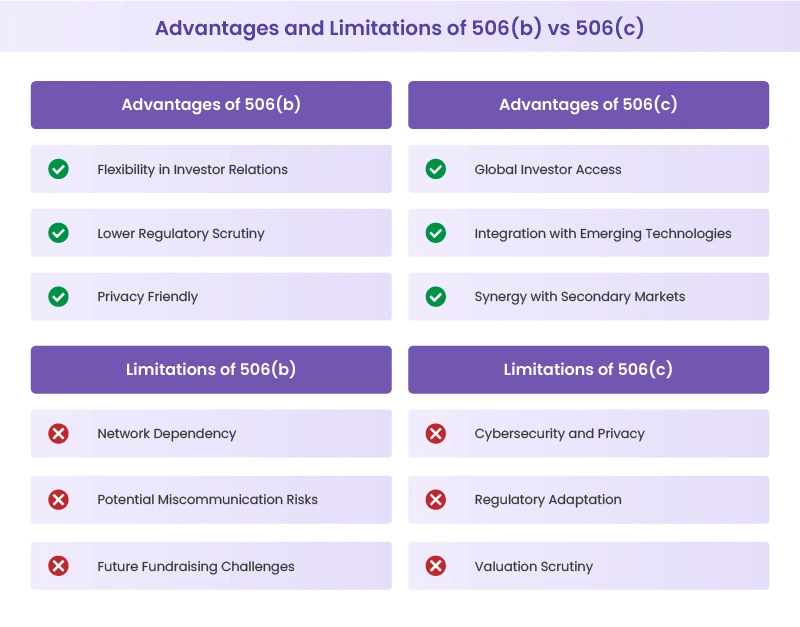

Let's have a look at the benefits and challenges associated with 506(b):

1. Flexibility in investor relations: This rule allows you to develop deeper relationships with a select group of investors. This leads to engaged stakeholders who also provide valuable industry insights and connections.

2. Lower regulatory scrutiny: Since 506(b) offerings are not publicly advertised, they typically attract less regulatory attention compared to 506(c) offerings. This can mean fewer compliance requirements for your startup.

3. Privacy friendly: If you are working on a disruptive technology or business model, 506(b) allows you to raise funds without alerting competitors through public advertisements.

1. Network dependency: Your fundraising success heavily relies on the strength and reach of your existing network. This can be challenging for first-time founders or those outside major startup hubs.

2. Potential for miscommunication: The prohibition on general solicitation practices means you must be extremely careful in how you discuss your fundraising efforts. Even casual mentions at public events or on social media could be seen as non-compliant.

3. Future fundraising complications: If you include non-accredited investors in a 506(b) round, it may complicate future rounds, especially if you are looking to transition to 506(c) or consider a public offering down the line.

Rule 506(c) under Regulation D allows startups to raise capital through general solicitation and advertising, a significant shift from the restrictions of 506(b). This rule will enable you to publicly promote your offering, making it possible to reach a broader pool of potential investors, provided they meet specific accreditation standards.

To comply with Rule 506(c), every investor must have an accredited investor status. You are required to take reasonable steps to verify the accredited status of these investors, which goes beyond the self-certification allowed in 506(b) offerings. Unlike 506(b), this rule excludes non-accredited investors entirely, streamlining the process for engaging with high-net-worth individuals and institutional investors.

The SEC provides several methods for verifying Limited Partner (LP) accreditation under 506(c):

Thorough documentation of the verification process is crucial, as, according to SEC guidelines, you bear the burden of proof.

Let's have a look at the benefits and risks associated with 506(c):

Challenges

Here are the key differences between Rule 506(b) vs Rule 506(c):

Rule 506(b) maintains a traditional approach, prohibiting general solicitation and advertising of your offering. This means you rely on existing networks and relationships to find potential investors. You might leverage private meetings, invite-only events, or personal introductions to connect with prospective backers.

In contrast, Rule 506(c) opens up new avenues for investor outreach. You can advertise your offering publicly, use social media campaigns, or even present at pitch events. This broader reach is beneficial for startups in niche industries or those looking to tap into a wider investor pool.

Rule 506(b) offers flexibility in your investor base. You can include up to 35 non-accredited investors, provided they are sophisticated enough to evaluate the investment opportunity. This can be beneficial if you have knowledgeable individuals in your network who do not meet the accredited investor criteria but could still bring value to your startup.

Rule 506(c), on the other hand, restricts your investor pool to accredited investors only. While this might seem limiting, it can streamline your fundraising process. Along with capital, accredited investors also offer industry expertise, valuable connections, and a higher tolerance for risk.

The investor verification process marks a significant difference between the two rules. Under 506(b), you can rely on investor self-certification. Essentially, investors can declare their accredited status without providing extensive documentation.

506(c) takes a more stringent approach. You must take reasonable steps to verify each investor's accredited status. This could involve reviewing financial statements, getting third-party verifications, or using other SEC-approved methods.

For 506(b) offerings involving non-accredited investors, you need to provide extensive disclosures similar to those in a registered offering. This includes detailed financial statements, risk factors, and information about your business and management team. The level of detail required can be substantial, potentially increasing your preparation time and costs.

506(c) offerings, limited to accredited investors, generally have more relaxed disclosure requirements. While you still need to provide sufficient information for investors to make an informed decision, the exact content and format are more flexible. This can allow for a more streamlined offering process, potentially reducing your legal and administrative costs.

Irrespective of which exemption you choose between 506(b) vs 506(c), you are still bound by anti-fraud provisions. This means all information provided must be accurate and not misleading.

Selecting the proper exemption between 506(b) vs 506(c) depends on several factors unique to your startup's fundraising goals and circumstances.

While choosing, you must also consider how your choice might impact future fundraising, as switching between exemptions in subsequent rounds requires careful planning.

The regulatory landscape surrounding Rule 506 is constantly evolving. The SEC has recently expanded the definition of accredited investors to include individuals with specific professional certifications, such as registered architects and certified public accountants. This could broaden the pool of eligible investors for both 506(b) and 506(c) offerings.

The SEC may implement stricter filing requirements and harsher penalties for non-compliance. For instance, there have been discussions about imposing a one-year ban on using Regulation D exemptions for issuers that violate the rules. Given the increased scrutiny and verification requirements, these potential changes might make some General Partners hesitant about using 506(c).

Navigating the complexities of Rule 506 offerings can be challenging. This compliance checklist serves as the roadmap to ensure you are meeting all requirements for your 506(b) or 506(c) offering.

This checklist helps you stay on track by outlining critical steps, from filing Form D and verifying investor accreditation to ensuring proper disclosures and record-keeping. By following this resource, you can streamline the fundraising process and minimize legal risks.

Download Link: 506(b) and 506(c) Compliance Checklist (2025 Edition)

Understanding the differences between 506(b) vs 506(c) is crucial for your startup's fundraising success. The final choice depends on your goals, investor network, and willingness to undertake additional verification processes.

At Qapita, we simplify this complex journey with our comprehensive equity management solutions. Our equity management platform, a market leader and top-rated equity management software by G2, is trusted by over 2,000 companies. We offer a suite of tools designed to streamline your equity management from inception to IPO.

Our CapTable Management system helps you track ownership, run scenarios, and effortlessly engage stakeholders. We also provide expert advisory and consulting services to guide you through the intricacies of compliance with Rule 506. Our team can help you structure your offerings to align with SEC regulations, whether you are opting for the traditional 506(b) route or exploring the general solicitation allowed under 506(c).

With ISO 27001 and SOC2 certifications, we ensure the highest level of data security for your sensitive financial information. Book a 1:1 demo today and learn more about our solutions.